Metro set to beat production guidance

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

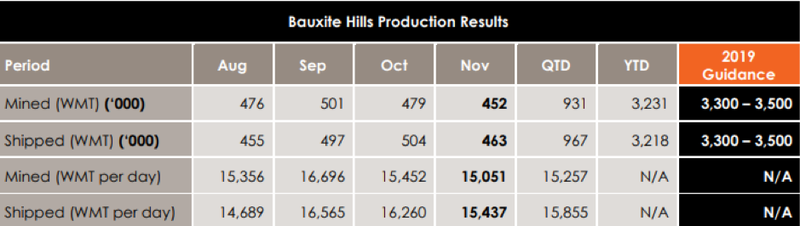

Metro Mining Ltd (ASX:MMI) could well exceed its yearly bauxite shipping guidance after another strong performance in November.

Pleasingly, management is taking a conservative stance with guidance, but mentioned that there was now a likelihood of meeting the upper end of guidance which is in a range between 3.3 million wet metric tonnes and 3.5 million wet metric tonnes (WMT).

If Metro can replicate its November performance, that would equate to 2019 production of nearly 3.7 million WMT.

Based on combined bauxite shipped in October and November, the average for the quarter is about 480 WMT per month.

If the company were to achieve at this level, the yearly shipment would be about 3.7 million WMT, a development that will be well received by investors and no doubt provide considerable share price support.

Commenting on the group’s performance for the full year, as well as the full-year guidance implications, Metro Mining managing director Simon Finnis said, “This is another very pleasing result for the team, both on and off site.

‘’We are on target to meet the upper end of guidance.

“It has been a very successful operational year and I am extremely proud of the effort and performance of the Metro team and our contracting partners.’’

Revenue generation to support Morgan’s price target of 35 cps

Interestingly, Morgans’ resources analyst Chris Brown ran the ruler across Metro Mining at the end of October.

At that stage he projected an above guidance performance, forecasting 3.6 million tonnes for fiscal 2019.

Based on these numbers, Brown expected Metro to generate a net profit of $22.1 million from revenues of $204 million.

This represents a PE multiple of 9 relative to Monday morning’s opening price of 14.5 cents.

While this appears to be extremely conservative for a company with an established operation and clear production and earnings visibility, the story is even more compelling based on 2020 metrics.

This will be the first year Metro will be producing at full tilt for the full nine month period between April and December 2020 inclusive.

Brown is forecasting the group to ship 4 million tonnes of bauxite in 2020, generating revenues of $237.8 million and a net profit of $42.1 million, representing year-on-year profit growth of about 90%.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.