Legal eagles ready to soar

Published 15-JAN-2019 11:06 A.M.

|

9 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

In recent years, a number of law firms have listed on the ASX, hoping to benefit from the amalgamation of smaller firms in what has historically been, for the best part, a cottage industry.

The most notable — or notorious in terms of destroying shareholder value — has been Slater and Gordon (ASX:SGH).

At its peak, the group was the largest ASX-listed legal services entity with a market capitalisation exceeding $1.5 billion.

Since its demise, the group has undertaken a one for 100 share consolidation initiative, illustrating the extent of the share price decimation that occurred after its attempted entry into the UK market went awry and questions arose regarding its accounting practices.

Today its market capitalisation is $163 million, and with a new board and a majority shareholder in Anchorage Capital Group charged with turning the business around, the company has received some rare share price support in the last week.

Management noted last week that in the past twelve months, the company has implemented a strong program of initiatives that it believes will provide a platform for long-term sustainability “so we can continue to unlock access to justice for the thousands of Australians who need our help.”

However, whether this resonates with the investment community remains to be seen as the destruction of capital was immense, and many retail investors — including those who are undertaking a class-action against the group — believe justice lies in recompense for their losses.

Should law firms be listed entities?

Even the ethics of legal services companies being listed entities has come under question.

Jeremy Roche, Attwood Marshall partner and Queensland Law Society accredited specialist in personal injury law, discussed the dilemma facing listed legal companies.

He noted that the recent financial problems experienced by Slater and Gordon highlight the ethical dilemma faced by public company law firms which have a duty to shareholders to maximise the profits/dividends and, arguably, “a competing higher duty to their clients to act in their best interests”.

Roche maintained that it was only natural to question the motives of a legal firm under such sustained financial pressure and to wonder if the clients’ claims are being properly prosecuted.

Pointing out that a consortium of hedge funds have now acquired 95% ownership of the equity of Slater and Gordon, Roche suggested that this would have an impact on the culture of the firm and its day-to- day operations.

Notwithstanding the events that occurred at Slater and Gordon, and, indeed, the flow-on impact that had on other ASX peers, we feel the time may be right to reassess the sector, while at the same time being cognisant of the need for strong management and a sound business model, as well as appropriate accounting procedures, particularly in terms of revenue recognition — an area that has come under intense scrutiny.

It could actually be argued that this was good for the industry, as companies now have to be careful regarding their assessment of likely future revenues, taking into account estimated fees, probability of success and percentage of completion.

The three companies we examine today are IMF Bentham Ltd (ASX:IMF), Shine Corporate (ASX:SHJ) and Xenith IP Group Ltd (ASX:XIP), with the latter specialising in all facets of intellectual property registration, management and protection.

IMF Bentham

Market cap: $610M

IMF is one of the leading global litigation funders, headquartered in Australia with offices in the US, Canada, Singapore, Hong Kong and London.

The company has built its reputation as a provider of innovative litigation funding solutions while establishing an increasingly diverse portfolio of litigation funding assets.

IMF has successfully led some of Australia’s largest class actions, but from an investor perspective, it is more the group’s decision to expand into new geographic markets, as well as broadening the areas of litigation it targets, that makes it an attractive prospect.

IMF has been a leading pioneer of litigation funding in Australia since 2001, playing a significant role in the initial steps towards a globalised industry via its international expansion.

The group has a highly experienced litigation funding team overseeing its investments, delivering as at 30 June 2018, a 90% success rate across 175 completed cases (excluding withdrawals).

In the company’s 17 years as an ASX-listed entity, it has successfully recovered $2.3 billion, out of which $1.4 billion was returned to funded claimants, with the company’s shareholders also benefiting from consistently strong dividends.

On this note, IMF has paid a dividend in every six month period for the last 10 years.

IMF's portfolio currently includes 75 investments, comprising 33 investments outside the US and 42 US investments.

The investment portfolio increased from an estimated portfolio value (EPV) of $2 billion to $5.6 billion as at 30 June and $5.8 billion as at 30 September 2018 — a useful lead indicator regarding the potential for growth in coming years.

It was only in mid-December that IMF completed a further US$125 million in capital commitments, bringing the capital raising for Fund 4 to US$500 million.

The group’s funds under management now exceed AU$1 billion, capital that will be used to finance litigation opportunities.

Management is aiming to have funds under management of $1.5 billion by the end of fiscal 2019.

In terms of generating returns on capital invested, the company’s strike rate is hard to beat, having won or settled 161 cases out of 179 contested in the last 17 years, generating revenues of $860 million, implying a return on invested capital of 150%.

The increase of approximately 170% in funding commitments between fiscal 2015 and 2018 can in part be attributed to the group’s diversification strategy.

In 2018, the banking Royal Commission took centre stage, and the Royal Commission into Aged Care Quality and Safety, which will span 2019 and 2020, could result in litigation, particularly given the degree of criticism the industry has received in recent years.

Shine Corporate

Market cap: $130M

While Shine Corporate has had its own share of internal issues over last three years, the demise of Slater and Gordon could have exacerbated the share price impact experienced by the group.

The last 12 months has been a rollercoaster ride for shareholders, with the company’s share price rallying more than 70% in the first half of calendar year 2018 as it increased from 62 cents in February to hit a 12 month high of $1.09 in May.

After hovering in a range between 85 cents and $1.00, even through the October rout, the company finally succumbed to global volatility in equity markets, recently trading as low as 67 cents.

However, there has been noticeable support in the last three weeks, with Shine’s shares rallying 10% as the market appeared to warm to the group’s acquisition of a majority interest in Carr & Co, announced in early January.

The $3.6 million acquisition will be debt funded, resulting in no earnings per share dilution, and, in fact, management expects the business to be earnings accretive in fiscal 2019.

The acquisition not only enhances Shine’s family law capabilities, but also strengthens the group’s position in the Perth market.

While not spectacular, it could be said that fiscal 2018 was a watershed year for the company in that it featured a continuation of acceptable levels of profitability, while delivering improved cash conversion and better returns on equity.

The group settled more than 6000 cases during the year, procuring damages in excess of $600 million.

Shine continued to execute on its diversification into practice areas in addition to personal injuries — most notably, class actions, family law, professional and medical negligence, land and environmental cases, dust diseases and abuse law.

The company is managing a class-action on behalf of AMP shareholders which was filed on the back of Royal Commission hearings.

The group has a particularly strong position in Queensland with 22 of its own practices, as well as those that operate under well-established brands in Brisbane and regional Queensland.

The company is also well-represented in New South Wales and Victoria, both in CBD and regional areas.

Prior to the Carr & Co acquisition, Shine was only represented in Perth and two regional areas of Western Australia.

Analysts at Morgans increased the company’s price target from $1.09 to $1.27 following its full-year result.

This implies a fiscal 2019 PE multiple of approximately 10 relative to the broker’s forecasts, suggesting there could be substantial share price upside from the company’s recent trading range, which is in the vicinity of 75 cents.

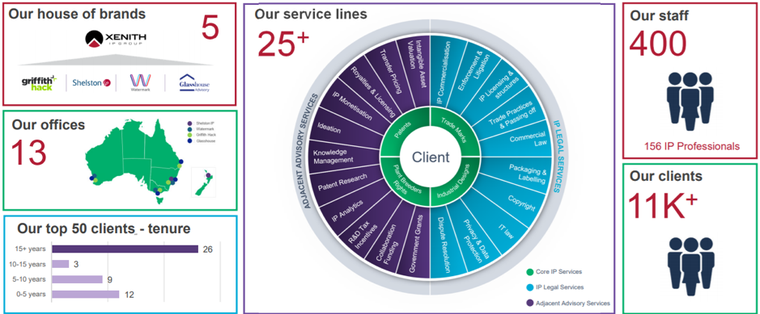

Xenith IP Group

Market cap: $117M

There also appears to be room for improvement in the share price of one of our other profiled stocks in the sector, Xenith IP, as it hovers in the vicinity of $1.30.

This compares with the recently updated consensus 12 month price target of $1.67.

Uncertainty regarding Xenith’s future could be contributing to its share price weakness as there is a three-way tussle between the group and two other players in the IP protection space — IPH Ltd (ASX:IPH) and QANTM Intellectual Property Ltd (ASX:QIP).

While Xenith and QANTM are looking to consummate a merger of equals, IPH is trying to crash the party by having a tilt at QANTM.

However, QANTM’s management has expressed its dissatisfaction with IPH’s non-binding, indicative and highly conditional nature of the acquisition proposal, saying only recently that the board and its advisers have determined that the proposed merger with Xenith creates shareholder value in the long-term as there is a strong cultural and strategic alignment between the two groups.

Should the merger go ahead — seemingly the most likely outcome from an operational perspective, given it is also strongly supported by Xenith — it would create the second largest IP management group in Australia by market cap. More importantly, it would have a dominant position in the domestic market.

The emergence of a highly competitive merged entity would no doubt be of concern for IPH, and arguably central to its sudden interest in acquiring QANTM.

Consequently, there remains a risk that the merger won’t go ahead as there is a price point (and albeit with acceptable terms) where the board of QANTM has to accept a prospective offer.

However, it should be noted that Xenith measures up well on a standalone basis, trading on a 2019 PE multiple of 9.2 as opposed to the industry average of 19.

The consensus dividend forecast is 9 cents per share, implying a yield of 6.8%.

As the dividend is fully franked, the grossed up dividend is 12.8 cents, implying a yield of nearly 10%.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.