A small company that sends the big guys packing

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

It was only Wednesday of this week when coronavirus ramped up that the S&P/ASX 200 index (XJO) crashed more than 90 points or 1.5%.

It was mainly just a handful of gold companies that survived the rout, benefiting from the surge in the gold price to long-term highs.

However, the one sector that did show resilience was Consumer Staples with the XJO 30 Staples Index (XSJ) up 66 points to 12,927 points.

The XSJ is home to household names such as Woolworths, Coles and Metcash, as well as beverages groups Treasury Wine Estate, Coca-Cola Amatil and the A2 Milk Company.

This suggests that the sector’s safe haven more defensive status could still be in investor’s sights, and certainly with the threat of coronavirus far from over, investing in stocks that are mainly leveraged to essential services spending still makes sense.

However, one of the not so attractive features of the sector is the premium multiples that these companies attract, predominantly because they have a strong market share with reasonable barriers to entry, and as we said earnings predictability.

It is worth noting though that these barriers to entry have been tested in recent years with Woolworths and Coles no longer being a virtual duopoly following the entry of other chains such as Aldi and Costco.

There is also plenty of competition in the alcoholic beverages space, particularly in wine, beer (increasing penetration of craft beers) and pre-mixed alcoholic drinks.

Even if you look through lower anticipated earnings in fiscal 2020 to fiscal 2021, you’ll find that both Coles and Woolworths are trading on PE multiples of about 25 which can’t be justified on an earnings per share growth basis.

Buying staples exposure at a cheaper price

My stock of the week is trading on a PE multiple of less than 10 despite having a strong growth outlook and exposure to the consumer staples sector.

Take a walk around any grocery store and you will find numerous products on the shelves that have been handled by this company, either individually or in bulk packages.

Granted, the company doesn’t produce or sell items such as milk, bread, wine or soft drinks, but as a prominent player in the fast-moving consumer goods packaging industry, they have strong relationships with those that do.

My stock of the week is Pro-Pac Packaging Ltd (ASX:PPG), a company that made an outstanding recovery as broader markets picked up following coronavirus.

PPG’s share price increased nearly four-fold from 6 cents to hit a high of 23 cents, a level it hadn’t traded at since 2018.

Looking at macroeconomic conditions, if the performance of companies such as Amazon is any indication, there could be a sustained increase in demand for packaging goods and services.

Institutional support from value-based investor

Recent volatility has seen PPG retrace to 16 cents, making it look very attractive.

Institutional investor Investors Mutual Ltd took the opportunity to top up its holding in May at levels of around 12 cents per share.

But well before coronavirus emerged, Investors Mutual identified the company as a quality undervalued story, buying large chunks of stock in 2018 at levels in excess of 30 cents per share.

As a long-term holder shareholder that promotes itself as a ‘’conservative quality and value-based investment style with a long-term focus aiming to deliver consistent returns for clients’’ this represents a strong endorsement.

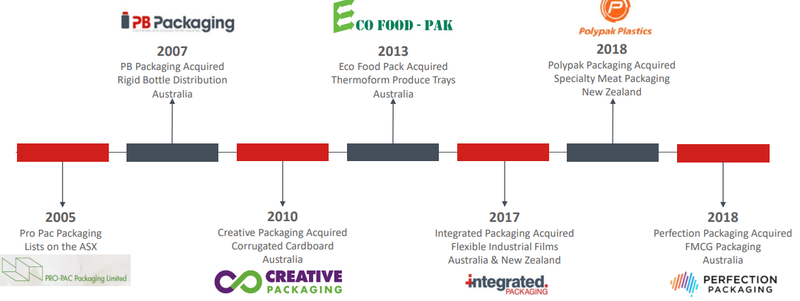

Robust institutional support has been important for PPG as it has been a growth by acquisition story as shown below.

Acquisitions provide scale and diversification

While PPG was established in 1993, it only listed on the ASX in 2005.

The best way to describe PPG’s performance over the last 15 years is that it is a company that has demonstrated consistency and a willingness to grow at a measured pace, while always looking for strategies that can be employed to improve the business.

For example, in the last three years, the company has grown rapidly as it more than doubled revenues, and is on track to generate EBITDA of $30 million in fiscal 2020.

PPG’s track record of generating a net profit every year since listing on the ASX is no mean feat for a company that is capped at around $130 million.

However, the company has experienced growing pains as is often the case when investing in new businesses with costs often placing a drag on earnings during the integration phase.

In my mind, PPG is at an inflection point where management has achieved significant debt reduction, cost-cutting and other measures to rationalise and right-size the business.

This is evidenced not just in the raw numbers such as debt reducing from $83 million at June 30, 2019 to current levels of around $60 million.

The upshot of these achievements has been a significant improvement in margins, a function of improved operational efficiencies and procurement savings.

The company is on track to achieve further debt reduction while achieving working capital improvements in fiscal 2021.

Looking across the divisions

PPG’s packaging business spans three areas - flexibles, industrial and rigid.

Flexibles is the dominant revenue generator, and PPG’s Australian and New Zealand manufacturing and distribution network provides flexible packaging solutions specifically tailored for the industrial, food and beverage, health and agriculture sectors.

In the first half of fiscal 2020 this area of the business accounted for 61% of revenue, up from 57% in the first half of fiscal 2019.

However, this is the area of the group’s business that has benefited greatly from improved efficiencies and a reduction in overheads, resulting in a significantly higher proportionate increase in EBITDA from 63% of underlying group earnings to 76%.

While this division incorporates an integrated recycling operation, as indicated below it has a substantial position in the grocery goods business.

The industrial packaging area of PPG’s business accounted for 27% of revenues in the first half of fiscal 2020.

It is a one-stop shop for primary, secondary and tertiary packaging with deep expertise in food, beverage, agriculture, retail and health sectors.

PPG’s point of difference in this area is that it is a provider of innovative solutions to the manufacturing and industrial industries rather than simply going through the packaging process.

This has been instrumental in positioning it as a key sourcing partner to global supermarkets.

While the rigid packaging business only accounted for revenues of 12% in the first half of fiscal 2020, its EBITDA contribution was 18%.

Management sees new business opportunities emerging in food and beverages, as well as emerging domestic health and well-being segments.

This area of the company’s operations should benefit from improvements in plant efficiencies and consolidation of sourcing in fiscal 2021.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.