MZI Resources flags improved production and price increases in 2017

Published 18-JAN-2017 13:33 P.M.

|

2 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

In the course of providing its quarterly activities update for the three months to December 31, 2016, mineral sands producer MZI Resources highlighted a number of records achieved for the quarter and suggested increased production from its Keysbrook project in Western Australia and an improved pricing environment would assist in driving revenues in 2017.

Reflecting on the three months to December 31, 2016, one of the most promising achievements was a 21% increase in the group’s production of high-value L88 leucoxene product.

While port congestion delayed a planned shipment of lower value L70 leucoxene in December, the benefits of this will fall into the March quarter.

It should be noted, however, that any further catalysts are speculative at this stage and should not be taken as guaranteed. Investors should seek professional financial advice for further information.

Production improvements sustainable

From an operational perspective, one of the key outcomes was the material improvement in overall production and on this note MZI’s interim Managing Director, Steve Ward said, “The December quarter was one of special significance for MZI, during which the Keysbrook Wet Concentrator Plant (WCP) achieved critical design performance milestones following the recently completed optimisation project”.

Ward noted that the optimisation project had quickly proven its worth and that the improved production was sustainable, validating the group’s investment.

MZI expects that the improvements at Keysbrook should flow through to the performance of the company’s Picton mineral separation plant when the next processing campaign commences in late January.

Industry conditions improving

Commenting on industry dynamics, Ward said, “Importantly, Keysbrook is starting to hit its straps at the right time, with the market outlook for mineral sands, including higher value products such as Keysbrook leucoxene, continuing to strengthen”.

On this note, MZI highlighted the fact that pigment producers are now seeing improvement in both volumes and price which is depleting inventory. Of further significance is the announcement of 13 rounds of price increases by Chinese producers in 2016.

Importantly for MZI, demand for chloride pigment has also resulted in reduced inventory levels and put upward price pressure on high-titanium dioxide feedstock such as rutile and leucoxene.

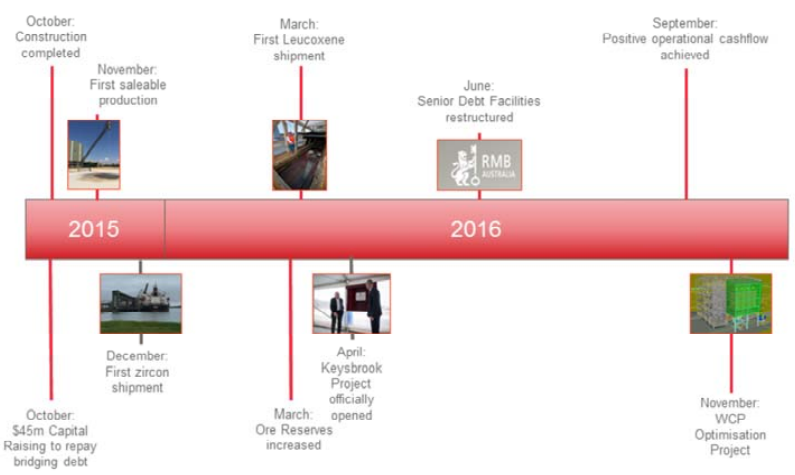

Here are MZI’s milestones for the past 12 months:

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.