Metro Mining generates EBITDA of $22.3 million in September quarter

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Metro Mining Ltd (ASX:MMI) shipped approximately 1.4 million wet metric tonnes (WMT) of bauxite in the September quarter, exceeding budget by 13%.

The company generated $79.5 million from sales and underlying earnings of $22.3 million with strong cash conversion which saw the company finish the quarter with $43.5 million in cash and receivables, up from $29.5 million as at June 30, 2019.

Management confirmed that it was on track to meet 2019 production guidance in a range between 3.3 million and 3.5 million wet metric tonnes.

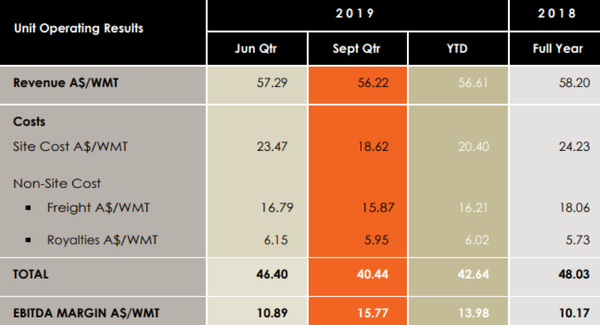

The company continues to receive strong prices for its product with $56.22/WMT broadly in line with the year-to-date average.

However, the real kicker from an operational perspective was the reduction in costs from $23.47/WMT in the June quarter to $18.62/WMT in the September quarter.

This was the first quarter in which the company has achieved underlying site unit costs of less than $20.00/WMT.

Management said that this was largely attributable to production exceeding budgeted levels and these economies of scale are anticipated to prevail for the remainder of the year.

The near term impact of a substantial increase in margins makes Metro even more compelling based on its current share price, but the broader issue of increases in scale driving profitability is well worth considering in terms of the company’s long-term investment merits.

Increased scale to drive near to medium-term earnings

On this note, subsequent to quarter end, Metro announced completion of the updated definitive feasibility study (DFS) for the Stage 2 Expansion of annual production to 6.0 million WMT by 2021.

The DFS has updated the capital cost estimate using experience to date and first principles to estimate operating costs.

It also included a review of the bauxite market conditions in China.

Under such a scenario, life of mine unit operating costs are forecast to reduce by approximately 18% delivered to China, which will increase operating margins.

This will position the Bauxite Hills Project in the lowest quartile of the global cash cost curve for bauxite producers.

A significant reduction in unit operating costs can be achieved by the use of a floating terminal that can load larger, ungeared ocean-going vessels including Cape Size vessels.

For a capital cost of $51.4 million it is estimated that Metro can be producing at a rate of 4 million WMT per annum by 2020, increasing to 6 million WMT per annum thereafter.

Management’s negotiations with debt providers are well advanced and a final decision to proceed will follow finalisation of the funding package and completion of the detailed engineering and design with the latter expected in November.

Consequently, substantial share price catalysts regarding the company’s near term expansion are imminent, and this combined with December quarterly production and sales could well see the company’s shares begin to reflect its robust financial position and growth prospects.

While management hasn’t changed its shipping guidance of between 3.3 million and 3.5 million WMT, maintaining the same run rate as that achieved in the September quarter would translate into shipped bauxite for 2019 of more than 3.6 million WMT.

Should management continue to outperform at the production and shipment levels while driving down costs, the much improved financial and operational metrics should also provide share price momentum.

Metro benefiting from owner-operator model

Given the factors that have contributed to the group’s impressive production and shipping rates will continue to benefit Metro, as we highlight below it would appear that the recent outperformance is sustainable.

Daily mining rates trended higher during the quarter, driven by high mechanical availability (+90%) of mining and haulage equipment and ore being sourced from both the BH1deposit and (closer) BH6 deposit, reducing the average haul distance.

Bauxite stocks at port and on water at quarter end were approximately 68,000 tonnes, leaving Metro well positioned to meet its production guidance.

The decision to move to an owner operator model continues to be highly successful generating the planned efficiencies and cost reductions across the business.

Blake Machinery Group, Metro’s equipment supply and services contractor, is performing as anticipated and the additional equipment available at site is providing greater operational flexibility.

Some engineering modifications at the Barge Loading Facility were completed to the overland conveyor system which resulted in record barge loading rates being achieved in September.

Transhipping activities are currently benefitting from good weather conditions and seasonal high tides which prevail towards the end of the calendar year.

With productivity of the crane operators continuing to improve with experience since operations commenced, and the return of Ocean-Going Vessels which have previously performed strongly, ship loading rates are now operating consistently above budget.

Imported bauxite prices remain resilient

Price and demand outlook for bauxite continued to be positive during the quarter despite the temporary closure of alumina refinery capacity in Shanxi Province after environmental audits by Chinese authorities.

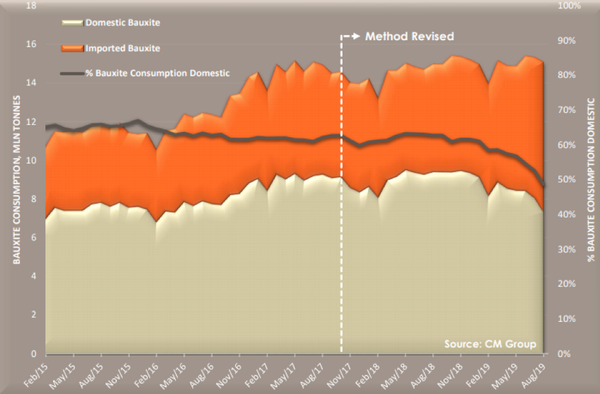

China’s August bauxite imports were down 4.5% to 8.6 million WMT (month-on-month) as output from Guinea fell, due to their wet season which disrupts loading operations, however the first eight months import total reached 71.3 million tonnes which was up 30.8% (year on year) reflecting strong demand from refineries.

Inland refineries have continued to diversify their bauxite supply and buy product from imported sources.

As a result, during August, total Chinese alumina production using domestic ore declined 9.1% month-on month.

As indicated below this is the first time that the proportion of production from domestic bauxite has fallen below 50%, and it is worth noting that it has fallen steeply since the start of 2019 when it accounted for 61%.

Imported bauxite prices CFR China, as measured by the CBIX bauxite index, remained near their recent year highs at US$50.70/DMT (dry metric tonne).

China’s domestic bauxite prices in Henan and Shanxi remained relatively stable with price support being generated from an increasingly strict environment policy in the lead up to China’s 70th anniversary celebrations, counterbalanced by increasing imports going to inland refineries.

It is difficult to see the landscape changing in terms of imposing stricter environmental regulations on domestic bauxite producers, potentially driving down the supply of local product, effectively increasing demand for overseas producers such as Metro Mining.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.