BW Equities bullish on BLK

Published 08-MAR-2016 12:51 P.M.

|

1 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

BW Equities Research has slapped a 75c 12-month price target on Blackham Resources (ASX:BLK), which represents a 54% uplift on its recent price.

The increased valuation come on the back of BLK recently putting out its Definitive Feasibility Study on its Matilda gold project.

That report, written for wholesale investors, confirmed production for this year with start-up of throughput and production likely to take place in the third quarter of this year.

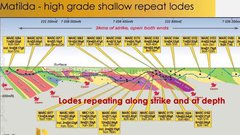

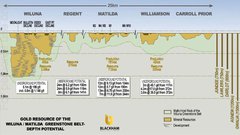

According to the DFS, BLK now has a mining inventory of 45 million tonnes of ore at a grade of 3.2 grams per tonne for 4.7 million ounces.

The surer indicated category makes up 21Mt @ 3.4g/t for 2.3Moz.

An extra 2.5 years was added to the project’s mine life from the project’s pre-feasibility study as well as a 44% increase in inventory.

At this stage it has a seven year mining inventory run planned, with the goal to produce 100,0000/oz per year.

When factoring in pre-production capital costs of around $32 million, BLK expects to hit around $234 million in cash flow and a net present value of $170 million.

The report’s author, Chris Bain, said the report’s price assumptions included a gold price of $1600/oz.

While the price of gold has been stronger in this in recent times, according to BLK’s PFS the price during the past five years was $1500/oz, but with forecasting notoriously difficult it is challenging to get a hard and fast reading on the gold price going forward.

Everything else about the project, however, is getting more solid as BLK approaches production according to Bain.

“Risks associated with the Matilda Gold Project are rapidly reducing as DFS work together with ongoing drilling progresses,” he wrote.

BW also projected revenue from the project, with Bain forecasting BLK to bag $117 million in the 2017 financial year – however forecasts continue to be estimates only.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.