Blackham continues fast paced development of Matilda project

Published 19-OCT-2016 16:52 P.M.

|

4 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Just a week after announcing that it had commenced gold production from the 5.1 million ounce Matilda gold project, Blackham Resources (ASX: BLK) has informed the market that the first gold pour has been completed, a significant milestone given the funding deal with Orion Mine Finance was only struck 16 months ago.

The group is now focusing on the ramp up and optimisation of the Wiluna gold plant with management indicating that both throughput and recovery are now underway with a view to maximising plant performance. In tandem with these developments has been a retracement in the group’s share price, and as broker reports suggest this may represent a buying opportunity.

From an operational perspective, mining from the open pits and underground has contributed to stockpiles greater than five weeks mill feed, positioning the group well to move to commercial production.

Of course it is not there yet, so if considering this stock for your portfolio take all public information into account and seek professional financial advice.

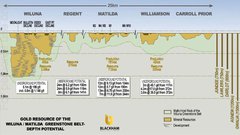

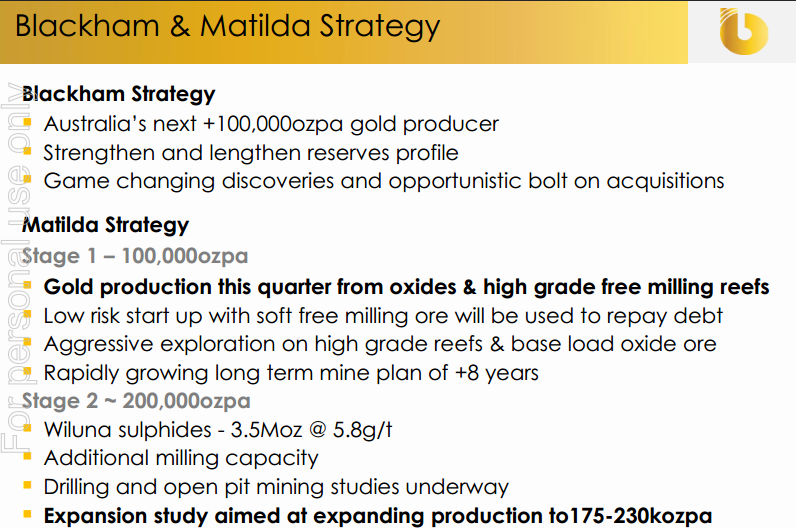

Looking at the broader picture, having quickly progressed to Stage I gold production, management is now fast tracking the second stage expansion study which aims to increase annual production to a range between 175,000 ounces to 230,000 ounces.

x\

While these developments have been well flagged by management, there was an interesting note released by Brett McKay from Petra Capital at the start of the month as he initiated coverage on the stock with a buy recommendation and a target price of $1.10.

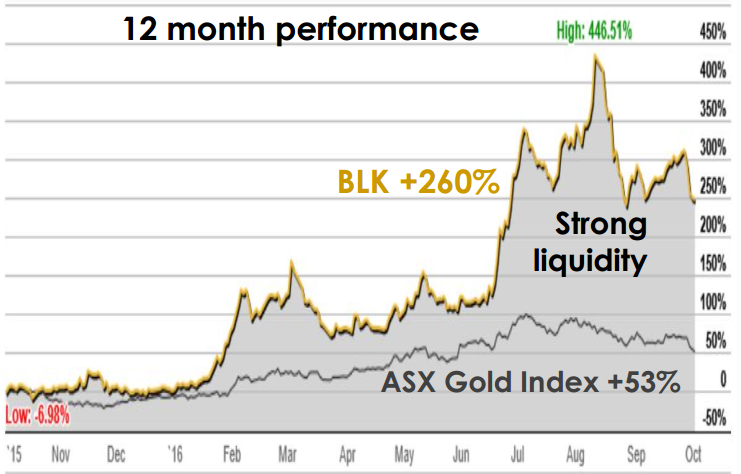

This implies a 47% premium to Wednesday morning’s opening price of 75 cents. BLK’s shares have come off substantially since hitting a high of $1.18 in mid-August, arguably driven by a mix of profit-taking and more recently, negative sentiment towards the gold sector.

However, it is worth noting that the company’s share price over the last three months is in sync with movements in the S&P/ASX All Ordinaries gold index. This raises the question as to whether the company should be trading in line or at a premium to the index.

As indicated by the 12 month share price performance against the gold index, investors have been attributing a significant premium based on the group’s promising outlook. This raises the question as to whether the stock has dropped off the radar because of broader negative sentiment towards the sector when the focus should be on its compelling medium to long-term outlook.

Given BLK’s production growth profile is superior to many of its peers it could be argued that a premium is appropriate. Certainly this is reflected in the consensus 12 month price target of $1.15, representing a slight premium to Petra Capital’s target.

While the pullback in the commodity price could see some downward adjustments in broker price targets, this remains to be seen. Petra’s earnings projections support its price target, particularly in fiscal 2018 when it expects production to exceed 100,000 ounces.

The broker is forecasting the company to generate a net profit of $50 million in fiscal 2018, representing earnings per share of 16 cents. This implies a PE multiple of less than five relative to this morning’s opening price.

More importantly though, it validates Petra’s price target which implies a PE multiple of 6.9.

Even though McKay hasn’t factored in changes in earnings from an updated reserve and mine plan which is expected to underpinned and expansion study in early 2017 he made some interesting comments on the potential impact of a change development plan.

Noting that ongoing drilling and studies are aiming to increase the mine life to around 6 to 7 years McKay said that the expanded project with four years of mine life adds 11 cents per share with each additional year of mine life adding a further 25 cents per share to the net present value.

McKay said, “The addition of extra milling capacity would allow the processing of both oxide and sulphide ore at the same time, thus lifting throughput to up to 2.7 million tonnes per annum for production of circa 200,000 ounces per annum over a shorter initial mine life of four years”.

It should be noted that broker projections and price targets are only estimates and may not be met. Also, historical data in terms of earnings performance and/or share trading patterns should not be used as the basis for an investment as they may or may not be replicated. Those considering this stock should seek independent financial advice.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.