ROG to Commence Crude Production in Colorado By November

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Red Sky Energy (ASX:ROG) stands on the verge of commencing maiden oil production at its newly acquired Cache Oilfield in Montezuma County, Colorado in the United States.

Following an Extraordinary General Meeting (EGM) held on July 17th 2015, ROG has finalised its planned acquisition of a 50% stake in the Cache oilfield, purchased from Monument Global Resources (MGRI), a management consultancy operating in the North American oil & gas industry.

As part of the transaction with MGRI, a highly credentialed team has also joined ROG. This incoming oil team boasts over 100 years of combined industry experience, which will drive ROG’s strategy moving forward.

ROG acquired a 50% interest in the Cache Oilfield by issuing 1.369BN fully paid ordinary shares, priced at $0.001. Alongside the acquisition, ROG completed a capital raising of $1.74M via the issue of 1.74M million fully paid shares, priced at $0.001.

The deal effectively means that ROG has paid $1.75M for 50% of an actively producing oil asset, independently valued at $30M. MGRI retains the other 50% and will continue to operate the Cache field in tandem with ROG.

Through this acquisition, ROG is demonstrating its new operational strategy of acquiring assets with immediate production potential. ROG is actively seeking out robust assets in brownfields oil & gas projects that can operate profitably even given current oil prices, and moving quickly to acquire them.

Drilling in November

Given the company holds assets located on proven oil fields, ROG will now complete its first production well and be producing oil for sale by the end of November 2015. However permitting is now underway for two production wells with the second well to be completed in 1H 2016. In selecting the first two sites ROG has taken advantage of the extensive amount of technical data as well as the incoming deep local experience of Cache.

ROG’s independent consultant forecast this first production well to operate for a minimum of 10 years and be producing between 250-500 barrels of oil per day (BOPD), with a preferred production rate of 350 BOPD. The Cache Oilfield is estimated to have approximately 5 million barrels still recoverable.

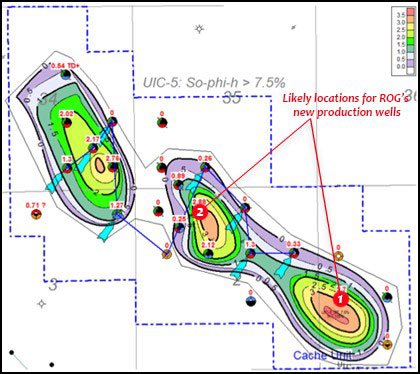

Early indications are that ROG will locate its two wells at the most optimal sites based on likely oil pressure and historical drilling data.

The two most likely locations are shown above with one new well expected to be drilled in the centre mound and one in the southern mound.

The southern location is a probable target based on the likelihood of ‘virgin’ oil pressure being high considering the comparative lack of historical drilling or fieldwork. Furthermore, there is good control data provided for the No. 15, 16 & 17 wells but of particular focus is the 16 well which was a consistent producing well prior to being plugged prematurely due to mechanical failure.

The second well is likely to be drilled in the centre mound which has the highest amount of productive wells in Cache. The centre mound is a likely target because the additional data available gives ROG the best chance of attaining sustainable flow rates.

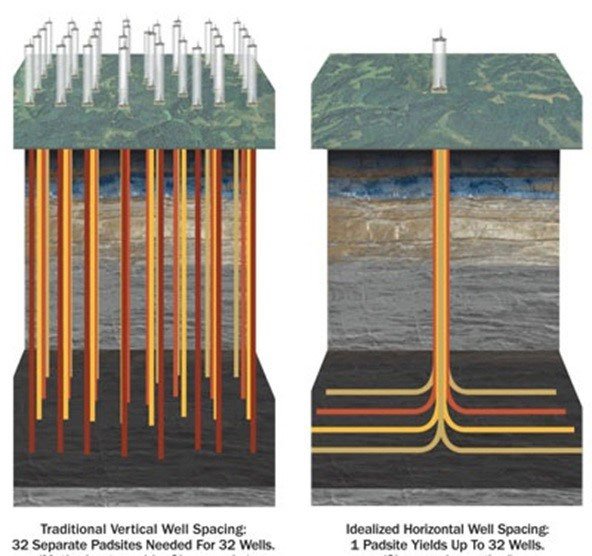

ROG intends to take advantage of modern horizontal-multilateral drilling to enhance its rate of oil production far beyond that of the original wells. By drilling laterally within the reservoir intervals, ROG is confident it can maximise the probability of intersecting zones of higher porosity and permeability leading to higher sustainable oil flow rates.

The graphic above illustrates how lateral drilling can be more effective and less ‘wasteful’ compared to standard vertical drilling. The Cache Oilfield has never been exposed to lateral drilling techniques.

Orchestrating ROG’s Strategy

As part of ROG’s 50% acquisition of Cache, the company obtains the services of three key figures, expected to lead the development of the Cache oilfield henceforth.

Mr Kerry Smith is the founder of MGRI and possesses over 30 years’ experience in a range of specialisations including data interpretation, usage of sophisticated drilling methods and resource evaluation. His most valuable attribute for ROG could be his forte of enhancing oil & gas production rates.

A key technical addition to ROG’s management team is Mr. William Reinhart. Mr. Reinhart brings with him a 36 year geology and geophysics background that has seen him gain extensive geologic experience across the U.S including a senior position with Mobil Exploration.

Also joining ROG’s management team is Mr. Ed Coalson, having been recruited as a project consultant. Mr. Coalson has over 40 years’ experience in geology and geophysics, working on a wide range of projects at U.S-based companies such as Coyote Oil & Gas Company, Strike Oil & Gas, LLC, Vecta Oil & Gas Company, Ltd., Cabot Oil & Gas Corporation, Bass Enterprises Production Company, and American Hunter Exploration Company.

All in all, the incoming team has over 100 years combined experience in, locating, evaluating and developing oil and gas interests in the United States.

With a new direction for the company now having been set, and a new management team also in place, ROG is already weighing up three more potential acquisitions to add to its North American portfolio.

ROG Director, Russel Krause was understandably tight-lipped about which assets are in his sights although he did confirm that natural gas assets are also being considered. Mr Krause commented, “The board is delighted to have completed the first acquisition under its new strategy to develop a quality onshore conventional oil and gas portfolio. The strategy is to acquire existing producing oil and gas fields which have been underexploited and whereby modern techniques can enhance production. The success in horizontal drilling of oil resources, along with CO2 injection techniques used in older fields has shown that production can be increased and significantly extended”.

Moving forward, the Cache field is expected to “provide an excellent platform from which to restore shareholder value as well as execute the board’s broader asset strategy of expanding the Company’s in-ground reserve”, added Mr. Krause.

A change of tides and a change of direction

ROG’s strategy has changed and for good reason.

Crude oil prices have fallen from grace above $100pb merely 1 year ago to $47pb today.

In a low oil price environment, ROG’s counter-cyclical approach hopes to acquire proven assets for cents on the dollar – with a view of maximising commercial value once oil prices rise. The reasoning is that once oil prices improve, ROG’s return on investment will be even higher having bought its assets during a ‘dip’ phase.

Another good reason to look for undervalued assets amidst low oil prices is because development drilling costs are also at historical lows. The cost of drilling a new well has fallen sharply alongside falling oil prices which further highlights the case for securing conventional, low-cost projects that don’t encroach on already squeezed margins amongst all oil producers globally.

Low oil prices tend to reduce drilling costs – at $100pb drilling a new production well typically costs $1M-1.5M. At $75pb the cost is approximately $1M. At $47pb, the well cost is anticipated to be below US$800,000 for its next well.

Given ROG’s $18pb cost price, as forecast by the independent valuer of Cache, the Company can generate a good profit on each barrel despite the current drop in oil prices oil prices.

Summing up, at this stage of the cycle, a low oil price helps ROG to acquire new assets at a discount, drill new wells for a relatively lower cost and therefore achieve competiveness savings compared to unconventional, high-tech and expensive oil producers that use techniques such as fracking.

As a listed ASX company focusing on crude oil, ROG is taking up a position to take advantage of the current downturn in oil prices using its counter-cyclical portfolio building approach.

With Cache now acquired and production to commence in the coming months, ROG is looking odds on to develop into a robust oil producer with significant acreage and most importantly, profitable production across several projects sites in North America.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.