EverBlu sees 300% upside in BPH

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The oil price has recovered most of the ground lost in September when it declined from about US$68 per barrel to US$58 per barrel.

In a sustained run since the start of October, the oil price has rallied approximately 10%, and it appears to be going through a period of stabilisation, trading comfortably above the mid-point of the extreme lows (US$30 per barrel) and highs (US$85 per barrel) that have prevailed in the last five years.

Some of the major players have already run on the coattails of this trend with Woodside Petroleum (ASX:WPL) outperforming the oil price as it surged 13% in eight weeks.

Santos (ASX:STO) is up by similar amount with the other major, Oil Search (ASX:OSH) just shy of that mark.

EverBlu Capital research analyst Russell Wright released a report yesterday suggesting there may be much better upside to be had by stepping outside the blue chips - in fact, well outside.

Wright believes that the $3 million BPH Energy Ltd (ASX:BPH) has promising prospects with the ability to capitalise on the development of one or some of the assets held by Advent Energy, an oil and gas exploration group in which it has a stake of 22.6%.

His implied share price target of 0.4 cents which also includes ascribed valuations for companies in other sectors such as medical devices implies upside of 300% to Thursday’s closing price.

BPH offers onshore/offshore diversification

One of the most attractive features of BPH’s interests is its diversification by geography and commodity, as well as offering exposure to both onshore and offshore oil and gas.

The latter is important for a smaller company such as BPH as it is much less capital intensive to drill and develop onshore projects than conducting deep water exploration and rig construction.

It is also worth noting that Advent’s portfolio of energy assets includes licences where contingent resources have been established.

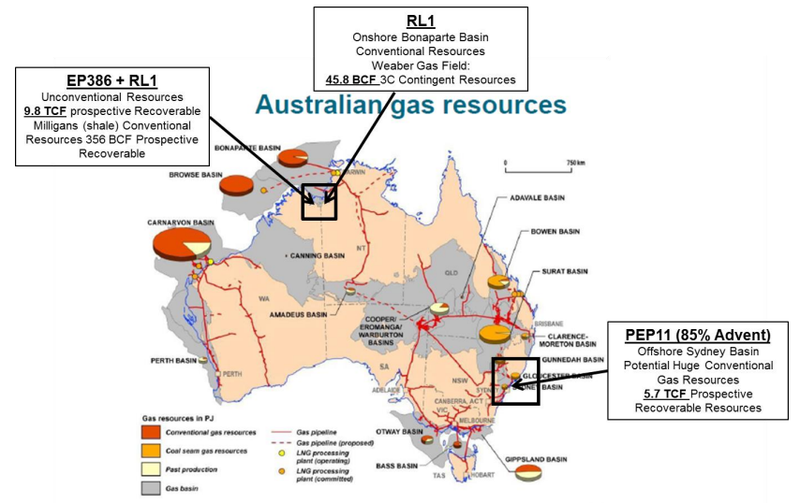

For example, in the Northern Territory Advent holds Licence RL1 (166 square kilometres in area), which covers the Weaber Gas Field, originally discovered in 1985.

Advent has previously advised that the 2C Contingent Resources for the Weaber Gas Field in RL1 are 11.5 billion cubic feet (Bcf) of natural gas following an independent audit by RISC.

The other asset is EP386 which has a recoverable resource estimates range from 53.3 Bcf (Low) to 1,326.3 Bcf (High) of Prospective Resources, with a Best Estimate of 355.9 Bcf of gas.

Significant upside 3C Contingent Resources of 45.8 Bcf have also been assessed by RISC.

The rapid ongoing development of the Kununurra region in northern Western Australia, including the Ord River Irrigation Area phase 2, the township of Kununurra, and numerous regional resource projects provides an exceptional opportunity for Advent to potentially develop its nearby gas resources.

These assets are located onshore in the Bonaparte Basin, and Wright highlighted that this is a highly prospective petroliferous basin, with significant reserves of oil and gas.

Most of the basin is located offshore, covering 250,000 square kilometres, compared to just over 20,000 square kilometres onshore.

With significant regional resource projects being conducted in the area, Wright pointed to market studies that have identified a current market demand of up to 30.8 TJ per day of power generation capacity across the Kimberley region that could potentially be supplied by Advent Energy’s conventional gas projects in EP386 and RL1.

Sydney Basin PEP 11 is the main game

While Wright acknowledges the potential of the Northern Territory and Western Australian assets, he sees Petroleum Exploration Permit 11 (PEP 11) as the group’s cornerstone project.

The permit which covers 8,250 square kilometres is located in the Sydney Basin which he sees as containing all the elements seen in other producing world-class structures.

Importantly, it is in close proximity to Australia’s largest energy market and extensive gas infrastructure.

As a backdrop, Advent assumed operatorship of PEP11 in 2008 and has since generated an extensive accumulation of data demonstrating an active hydrocarbon system in what is considered a proven petroleum basin.

The permit has recently been estimated to contain 13.2 trillion cubic feet (TCF) prospective recoverable gas resources (at the P50 or ‘best estimate’ level).

Advent has conducted a focused seismic campaign around a key drilling prospect in PEP11 at Baleen, in the offshore Sydney Basin.

The high resolution 2D seismic survey covering approximately 200-line kilometres was performed to assist in the drilling of the Baleen target approximately 30 kilometres south-east of Newcastle, New South Wales.

A drilling target on the Baleen prospect at a depth of 2150 metres subsea has been identified in a review of previous seismic data.

Intersecting 2D lines suggest an extrapolated 6000 acre (24.3 square kilometres) seismic amplitude anomaly area at that drilling target.

Advent is now evaluating contracting semi-submersible rigs to drill the Baleen well to evaluate a target of multi-TCF size.

Taking all these factors into account, Wright values BPH’s share of Advent’s energy holdings at approximately $1.4 million.

BPH’s investments value at more than $5 million

As Finfeed discussed earlier in the week, BPH also has a 4.56% stake in medical device group Cortical Dynamics which could be increased to at least 14% at this stage.

Cortical is an Australian based medical device technology company that has developed an industry disruptive brain function monitor independently described as “a paradigm busting technology from an Australian based device house that really gives a significant advantage in this space”.

The core product, the Brain Anaesthesia Response (BARM) monitor, was developed to better detect the effect of anaesthetic agents on brain activity, aiding anaesthetists in keeping patients optimally anaesthetised.

Cortical has received both TGA approval and the CE Mark and has now commenced its sales campaign.

Wright explained that a capital restructure could see BPH’s stake in Cortical Dynamics rise to 19.7%, and he concluded that in such circumstances a valuation of $3.15 million could be ascribed to BPH.

This is how he crunched the numbers:

A simple way to value Cortical Dynamics is to recognise that they are currently seeking to raise an extra $2m through issue of 20,000,000 shares at a price of $0.10.

Provided this equity raise is successful, then Cortical Dynamics’ total outstanding shares will increase to 133,353,431 at a market price of $0.10, providing an estimated market value of $13.3 million.

In addition, BPH and Grandbridge Limited are seeking Cortical shareholder approval (at their 29 November AGM) for the conversion of $2,653,586 in debt into 26,535,857 Cortical shares.

Provided this equity raise is successful, then Cortical Dynamics total outstanding shares will increase to 159,889,288 at a market price of $0.10, providing an estimated market value of $16 million.

Moreover, BPH’s post-raise shareholding would rise from 4.39% to 19.73%.

Given this BPH shareholding of 19.7%, their ownership of Cortical Dynamic can be valued at $3.155 million.

Patagonia offers unique cannabis strains

Wright values BPH’s holding in Patagonia Genetics at $500,000, bringing his total valuation to $5.05 million which provides the foundation for the share price target of .04 cents.

Patagonia Genetics is a craft cannabis company based in Patagonia, Chile boasting a genetic collection of over 260 unique cannabis and hemp strains, carefully collected from industrial hemp cultivations of the late 1980's whose germination rates were verified in late 2016 with knowledge of the Livestock & Agriculture Service (SAG).

Patagonia Genetics boasts a Chilean gene pool that has remained greatly isolated from international markets until recently, whilst a large proportion of its unhybridized landraces haven’t been seen in domestic markets for over 30 years.

Patagonia’s physical collection of 30,000 seeds includes a variety of hemp and cannabis strains that have been selected for their exceptional terpene profile, production yield, pest resistance, uniqueness, CBD/THC content, and medicinal properties.

Ten Latin American (LATAM) countries have legalised cannabis for medicinal usage and three have decriminalised adult use.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.