88E’s resource more than doubles at Icewine

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

DeGolyer & MacNaughton thinks 88 Energy (ASX:88E) may have up to 1.4 billion barrels of recoverable oil equivalent on its hands at Icewine, but internal figures have that number at up to 3.6 billion barrels.

The ASX-listed oiler released the first set of numbers on the Icewine project since it finished drilling, with the bulk of technical analysis on Icewine-1, showing 88E tripled its acreage position in the area.

According to independent assessor DeGolyer & MacNaughton, the Icewine project could have between 255.7 million barrels of total liquids and the play and 1.9 billion barrels of total liquids.

Before drilling at Icewine-1 began, D&G had put the recoverable potential of the play at 492 million barrels on a gross mean unrisked basis.

Some of the liquids at the project are wet gas, with 88E converting this into oil equivalent to come up with the 1.4 billion barrel oil equivalent figure.

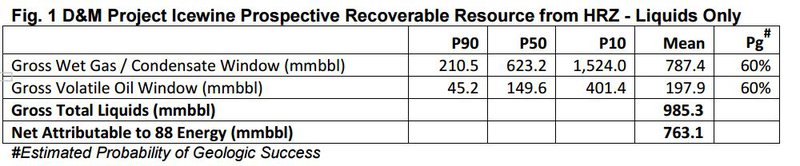

The mean prospective recoverable liquids was put at 985.3 million barrels.

D&G resource estimate

The consultancy also put the geological chance of success at 60%, up from its previous 40-41%, on the back of 88E’s extensive technical work at Icewine-1.

The company, however, thinks the consultancy may have underestimated the potential at the project.

It’s also put out a set of internal numbers for the project which beefs up the amount of land which may be production.

While D&G assessed all of the Icewine area in its calculations, it put the estimated productive areas at 42%, 88E has put out a more bullish 70% figure.

This leads to an internal resource estimate of 3.6 billion barrels of oil equivalent, with a mean of 2.6 billion barrels of liquids.

88 Energy’s internal estimate

88 Energy told its shareholders that the discrepancy was down to the various calculation methods both parties had used.

While D&G used a comparatively generic set of guidelines around statistical analysis of other shale plays at a similar stage around the world, 88E’s model was driven by on the ground experience at Icewine.

The main difference between the pair was the amount of Icewine land which was deemed to be productive, with 88E saying that its more bullish estimate was driven by “years of hands on experience with developing the Eagle Ford Shale” and its internal thermal maturity model – which was confirmed by the drilling of Icewine-1.

Despite the discrepancy, 88E managing director Dave Wall said in any case the upgrade was a good sign.

“The large upgrade to the resource potential at Project Icewine highlights the unique leverage that a project with this possible magnitude provides to investors,” he said.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.