A healthy six pack in a hot sector: Part 1

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

In light of the volatility that has rocked global equities markets including the ASX, Finfeed felt it was timely to assess the damage on a sector by sector basis.

What’s more, we have come up with six stocks that appear to have plenty going for them in fiscal 2020.

The old saying ‘don’t throw the baby out with the bathwater’ is often one to bear in mind when markets appear fragile.

Importantly, sectors that show resilience in the face of broader market headwinds often have more run left in them.

Targeting stocks in resilient sectors is generally a much healthier trend than riding on the coattails of a bullish sector, unsure of where it is going to peak and whether the underlying fundamentals really warrant the bullish sentiment.

Looking at the current conditions though, if you step back say five years it was hardly worth running the ruler across the sectors when times were tough.

You could be sure that the money would be exiting the market altogether or going into the banks or Telstra.

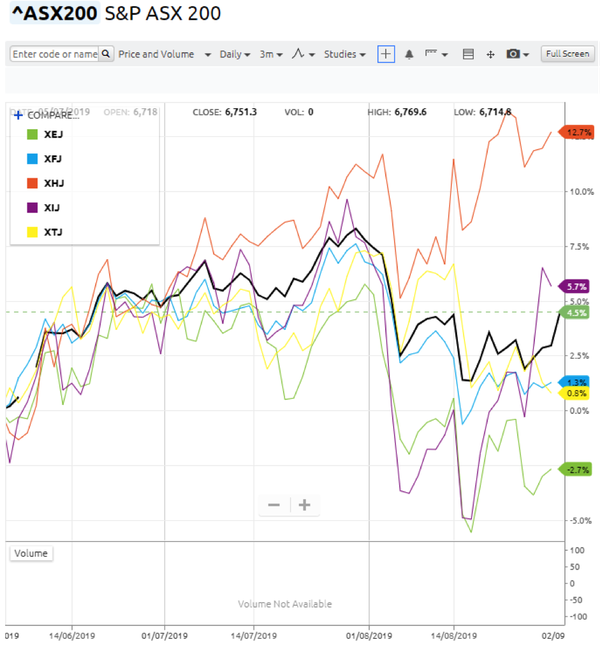

Today it is a different story as indicated in the three months chart below, which highlights the window between June and August.

Why this three month period? Because it captured the last two months of the strong run we had in calendar year 2019, while also showing where the traction was when the markets turned.

As you can see above, the S&P/ASX 200 Healthcare Sector (orange line) blitzed the rest of the market, increasing 12.7% against the ASX 200 (black line) which interestingly by the start of September was already back in positive territory, up 4.5%.

It is also worth noting that there was only one sector that hadn’t edged its way back into the black, and that was the S&P/ASX 200 Energy sector (green line), down 2.7%.

But the big change in dynamics is evidenced in the relatively poor performance of the ‘back in the day’ traditionally stronger S&P/ASX 200 Financials and Telecommunications indices, denoted by the blue and yellow lines respectively.

These two sectors were up 1.3% and 0.8% respectively, making them the only other sectors besides the energy sector to be underperforming the ASX 200.

The banking sector has come under pressure because of the Royal Commission which not only dented the credibility of the major banks, but eroded some of the areas that were generating the most growth.

With regard to Telstra, it is no longer the go-to yield stock that it used to be.

In fiscal 2014 the company paid an annual dividend of 29.5 cents, implying a yield of nearly 6% based on its share price as June 30, 2014.

In fiscal 2019 the company paid a dividend of 16 cents per share, implying a yield of 4.2% relative to its share price as at June 30, 2019.

Targeting emerging stocks in growth markets

Finfeed trawled through both large and small stocks in the health and biotech sector with a view to identifying stocks that fitted more in the ‘emerging’ category in order to target those that had the potential for significant share price upside.

We also looked to tap into key industry developments as a guide to which sub-sectors to focus on.

On this note, Bell Potter analysts John Hester and Tanushree Jain recently highlighted some important themes to be cognisant of in fiscal 2020, as well as putting forward their top picks in the sector.

Two of the six companies we present are favoured by Hester and Jain, but before we look at particular stocks it is worth gaining their insights into what they believe lies ahead for the industry in fiscal 2020.

This is an excerpt from a report they collated as fiscal 2020 was about to unfold which provides a window of about 10 weeks to assess how their take on the sector appears to be shaping up, a real litmus test given what a volatile 10 weeks it has been.

‘The fundamentals and demographic trends for the healthcare and biotech sector remained strong in FY19 and we expect some of the key themes from last year to continue to play out in FY20.

Friendly regulatory environment – We believe the US FDA will remain friendly and open to supporting companies through accelerated pathways to get medicines with unmet needs to market faster.

Licensing and M&A activity to remain high - We believe partnering activity will remain high as there is no shortage of cash-rich companies looking to acquire or license promising assets. Multi-billion dollar deals have been done in the US already which sets a positive tone globally. We also expect continued investment from China into the sector.

Further maturing of ASX listed biotechs - We also expect further maturing of companies we cover, with more trial readouts, potential partnerships and commercial launches throughout the year. Commercial momentum is expected to pick up for marketed products by medical device companies that are still in the initial stages of commercial rollout.

Oncology will remain a hot focus globally.’

Alcidion Group Ltd (ASX:ALC)

Shares in Alcidion Group (ASX:ALC) have performed strongly in the last six months, increasing approximately five-fold to hit a 12 month high of 21 cents last Friday.

Last week’s surge of 25% came after the company delivered its fiscal 2019 result which featured strong revenue growth and the group’s first full year of positive operating cash flow.

The company chalked up a number of achievements in fiscal 2019, including major new contracts for first combined Miya, Patientrack, Smartpage installations in Australia and the UK.

Management was also able to provide a strong outlook statement with the company having already generated $11.7 million in revenue in fiscal 2020, and a further $19.5 million contracted out to 2025.

Of particular note is the growing proportion of recurring income, providing financial stability and predictability of earnings.

Alcidion achieved several significant operational milestones in FY2019, signing or renewing approximately 90 customer contracts over the year, as well as generating a solid book of sold recurring and non-recurring revenue.

This included several strategically important contracts such as the first integrated Miya, Patientrack and Smartpage installations in both Australia and the UK, at ACT Health and Dartford and Gravesham NHS Trust respectively.

It has been a gradual build for Alcidion as it has acquired complementary businesses with technology platforms that now provide the company with an integrated service offering in the fast growing digital information and communications business segment.

In 2017, Alcidion acquired Oncall Systems and its Smartpage clinical communication system.

In 2018 , the company acquired the Patientrack bedside patient monitoring software and MKM Health, an IT solutions and services provider.

These offerings now operate under the Alcidion brand.

With over 25 years of combined healthcare experience, Alcidion brings together the very best in technology and market knowledge to deliver solutions that make healthcare better for everyone.

The company’s suite of products now offer a complementary set of software services that create a unique offering in the global healthcare market, including solutions that support interoperability, allow communication and task management, and deliver clinical decision support at the point of care to improve patient outcomes.

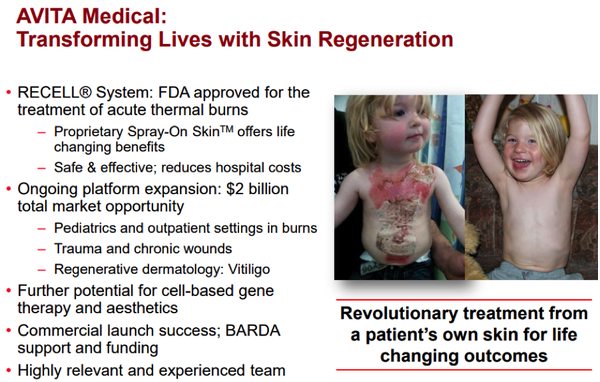

Avita Medical Limited (ASX:AVH)

Avita Medical Ltd (ASX:AVH) has been on Bell Potter’s key picks list since December 2018.

Avita and its subsidiaries are a regenerative medicine group with a technology platform designed to address unmet medical needs in patients with burns, chronic wounds, and aesthetics indications.

The company’s patented and proprietary collection and application technology provides innovative treatment solutions derived from the regenerative properties of a patient’s own skin.

Avita’s medical devices work by preparing a Regenerative Epidermal Suspension (RESTM), an autologous suspension comprised of the patient’s own skin cells that are necessary to regenerate natural healthy epidermis.

This autologous suspension is then sprayed onto the areas of the patient requiring treatment.

The first medical device based on the RES technology, the RECELL® System, was approved for sale in the US for the treatment of acute thermal burns in patients 18 and older by the Food and Drug Administration (FDA) in September 2018.

The company initiated its US national market launch of the RECELL System in January 2019, although it did commence commercial shipments in the US during the half-year ended 31 December 2018 in response to pre-launch demand from burn centres.

The RECELL System is also sold on a limited basis in certain regions of the world in which the products are approved for sale, including Australia, China and Europe.

Sale of goods of the RECELL System totalled $7.7 million for the year ended 30 June 2019, up 540% on 2018 sales.

The majority of the current fiscal year increase in sales occurred in the US as a result of the September 2018 FDA approval and commencement of the US national market launch of the RECELL System in January 2019.

US sales during the fiscal year ended June 30, 2019 totalled $6,214,660, and gross margins were a healthy 78%, a level management expects it can improve on further as sales ramp up.

Avita is one of Hester’s favoured stocks in the sector and he has a buy recommendation on the stock supported by a 12 month price target of 68 cents per share.

This represents a premium of approximately 35% to Friday’s closing price of 50.5 cents, although it should be noted that broker projections are speculative.

Consequently, even though the company’s shares have performed strongly over the last 12 months, it may not be too late to capture further upside in a stock that is forecast to grow revenues by about 400% over the next three years and be generating EBITDA of $28.5 million by fiscal 2022.

Imagion Biosystems - IBX

Similar to Alcidion and Avita shares in Imagion Biosystems have also been well supported recently, increasing approximately three-fold since June.

However, this has been off a relatively low base, suggesting there may well be further upside to come.

As a backdrop, Imagion Biosystems is developing a new non-radioactive and safe diagnostic imaging technology.

By combining biotechnology and nanotechnology, the company aims to detect cancer and other diseases earlier and with higher specificity than is currently possible.

A key development that has provided considerable interest in the stock was the designation by the FDA of its MagSense System and Test for staging HER2 breast cancer as a breakthrough device.

The purpose of the Breakthrough Device Program is to expedite and improve communications between a device manufacturer and the agency during device development.

On this note, executive chairman Bob Proulx said, "Qualifying as a Breakthrough Device validates our MagSense technology as a transformative opportunity for healthcare, and could improve the standard of care for staging HER breast cancer."

Another important development was the completion of a toxicology safety study of the group’s lead MagSenseTM nanoparticle formulation for the detection of HER2 metastatic breast cancer.

The study was completed on time and no adverse effects were reported.

The company’s early feasibility, first-in-human study is a critical milestone in the development of the company’s non-radioactive imaging technology which provides a non-surgical solution to identify the progression or stage of HER2 breast cancer metastases.

The MagSense test for the staging of HER2 breast cancer aims to eliminate the unnecessary surgeries and concomitant morbidity resulting from the current standard of care biopsy procedure.

Click to listen to an insightful podcast conducted with Proulx as he explains how Imagion is leading the way in bringing the industry into the 21st century.

Adding further to the Imagion story was news released on Monday that the company is progressing with a study where early stage results have demonstrated that the anti-HER2 nanoparticles used in Imagion’s MagSenseTM technology, which provide specific targeting of cancerous cells, may also have potential as an MR imaging (MRI) contrast agent.

Importantly, the study shows the MagSenseTM nanoparticles may be equally effective as a multi-modal molecular imaging agent, generating detectable signals in two different imaging methods - super magnetic relaxometry (SPMR) and magnetic resonance imaging (MRI).

Discussing the significant commercial relevance of this development, Proulx said, “While development of our proprietary magnetic relaxometry technology has been our focus to date, this new preliminary work shows the potential for our MagSenseTM nanoparticles to work with MRI and could open up a new commercial pathway as an contrast agent that can be used to improve the effectiveness of MRI in the detection and monitoring of HER2 breast cancer.”

That's three of the six healthcare stocks we are covering in this feature, join us tomorrow as we look at Lifespot Health Ltd - LSH, Prescient Therapeutics Ltd – PTX and Starpharma Holdings Ltd - SPL.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.