Q&A: Will the market recover post COVID-19 and what are the sectors we should be looking at?

Published 17-JUN-2020 12:21 P.M.

|

10 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The market fluctuations are hard to read and there have certainly been ups and downs, but what causes the dips and how can global economies recover?

Bourse Communication founder and Managing Director Rod North has been working within financial market since the 1980s and has seen pretty much all there is to see, from stock market crashes to the GFC, to the current pandemic, and past recoveries. He speaks with Jonathan Jackson about where the market is at and what we can expect as we come out of the pandemic.

Jonathan Jackson (JJ): Rod, thanks for joining us today. You’ve seen pretty much all there is to see, how does this COVID-19 crash compare with others?

Rod North (RN): Thanks very much, Jonathan, and yes, I think I’ve witnessed maybe five, nearly six booms and busts, so it's been very interesting to see what's been happening over the last six months and how that's all played relative to all those other booms and busts that we've seen, right back even to the 1979 and 1980.

JJ: What have been some of the more memorable events?

RN: Well, I guess probably one of the most defining was the 1987 stock market crash, because it really happened very, very quickly, and we saw a decline pretty much overnight on the 19th of October, 1987, by around 40 to 50%.

It basically wiped out an enormous amount of people's wealth overnight. I remember getting a call from my wife's grandfather, (who at that stage was in his late 80s) the day after the crash saying, ‘Rod, this is the time to buy’. And of course I was saying, ‘Well, maybe George, the whole world could come to an end, we're not sure. We'd better keep our powder dry’. But as it turns out, he was actually right on the money and reminded me for the subsequent years that I really should have not talked him out of buying shares at that particular point in time.

The market eventually recovered and took quite a while to reach its top in 2007, when we got to 6,800. Then the GFC hit. I suppose the difference with the GFC, was that that market dropped over a fairly long period of time, so it peaked in November 2007 at 6,800 and reached its bottom in March 2009, when the index fell to 3,109.

That was a decline of over 50% as well, and I suppose it's quite interesting, because when you look at the set of circumstances of all those other booms, of '79, '80, which was the resource boom and bust, the index has just continued to get higher and higher. At that point, it had got to a thousand for the first time. Then in 1987, we got to 2,800, and then through to 2007 to 6,800.

The interesting thing that's happened with the current coronavirus, COVID-19 market correction is we went from really a 10 year bull market up to February this year, when we peaked over 7000. I think we got to 7,200. And then we were hit by a Black Swan event, something completely out of the blue, unlike the other booms and busts, which were very much indicative of perhaps over evaluations in markets and other economic factors that came to play. This pandemic has created incredible havoc in the world, and we saw the markets drop through March/April to 40%.

Through May we've seen a building process that's seen the market recover, from under 5,000.

If you work out the percentages, from top to bottom, that really puts our market now only down 18.1% from the peak. So you could get people arguing, well hang on a minute, are we still in a bear market, or are we now in a bull market, because generally a bear market is indicated when a market is sustainably down by 20% or more. So it'll be really the test of time over coming weeks looking at how companies perform through to June 30 that's going to be the key.

JJ: Earning are vital?

RN: For all the years I've worked in funds management, and sat on investment committees at Colonial First State and Australian Unity and Norwich Union, the one key thing that always drove share prices up was earnings. And the biggest impact that we've seen in the history of the share market, at the moment, is trying to actually quantify the earnings effect that the coronavirus has had on so many of the two and a half thousand companies listed on the ASX.

There will be companies that are defined by this, that won't survive. And I said sometime back, that the CEOs that were running companies before 20 February this year when the market peaked, may not be the CEOs that are going to be running the same companies in six or 12 months. It's going to be a whole different paradigm, I think.

JJ: I do want to look at industries and companies to watch out for as we move along here, but I just wanted to take you back a little bit, and look at your career and why you got into the markets in the first place. Is it still as exciting, or more exciting for you now with everything going on?

RN: I think it's always been thrilling. I mean, my father was a stockbroker for 40 years, so it was very much in the blood. I used to go in from quite a young age to his stockbroking firm in Melbourne, from when I was probably six or eight, so it was a natural sort of fit after I completed my economics degree. I was also doing law, but I found just law to be a little bit onerous. The attractions of the market, particularly in the early '80s, was just way too entrancing for me.

I was working initially in share broking for many years, and then in funds management. I think the beauty of investment markets is that yes, there's so much happening every day, every week, every month, every year. You know, there's other things sort of coming to play on the micro, the macro level, the whole sort of geopolitical stage. When you look at situations like 20 years ago, we had the US as the most powerful country in the world, with Russia and China sort of nowhere near that.

The US had a demonstrable position as the biggest and most powerful country in the world, but in 20 years we've now got Russia and China competing at that sort of level as well, and it's changed the whole dynamics and geopolitical situation. Which becomes unpredictable. I guess in all my experience over the last 35 odd years, is that markets really don't like uncertainty at all. And one thing I would say, despite the fact that there may have been some green shoots appearing with the market getting back to over 6,000, and perhaps people thinking, oh, well this could be sort of a short term decline, and we might only be in a bear market for a short period of time, I think that uncertainty that we're faced with what's happening both in terms of the relationships with the US and China, and also what's happening in Hong Kong at the moment, does create a high level of uncertainty. That prevents people from moving out of cash back into equities.

JJ: Australia is currently in a fight with China. America is having a fight with China and there's a presidential election coming up. Do you think that sort of uncertainty will continue for some time to come?

RN: Yes, I do, and I think even when look back six or 12 months, we could say, well, the economies around the world were basically pretty sound. Australia wasn't looking like it had any chance of going into a recession. You know, there was a potential chance that we could have been in surplus, or certainly the budget would be balanced. The US had a very powerful economy with the lowest unemployment rate in a very long time, and a share market with the Dow at an all-time high. Singapore is going into a recession for the first time in 50 years. It just shows you how things can very much turn on a dime. Governments have had to throw billions of dollars at this market and we really don't know what's ahead of us, other than we do know that it is very likely that Australia will go into a recession for the first time in 50 years.

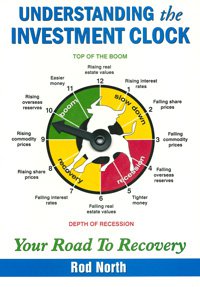

JJ: In terms of your book, Understanding the Investment Clock and the philosophy behind that, where are we sitting?

RN: I think we're clearly in the recession phase. We reached the top of the market, which was midnight on the 20th of February. I think we were all rather hopeful that the party might have continued for a bit longer. And I think when the party was over, we saw the market move out of that boom phase into what is the recessionary phase, which sort of takes us through to around 2 to 2:30 on the investment clock. That now has to play out as to whether we come out of that relatively quickly or it's going to take six to 12 months.

There are also macro events to consider in this. Two months ago, President Trump looked like a shoe in to be re-elected in November for a second term of four years. Now, with the BLM movement and a pretty formidable candidate in Joe Biden, who was the Vice President for two terms, that contest is going to be a tough one. And the ramifications of that, if America ends up in the hands of the Democrats again, could be a whole different economic rationale compared to what the Republicans are like in terms of growing and building business, and supporting small and bigger enterprises. I think, we are going to be very volatile over the course of the next six months.

JJ: Will we come out of this period?

RN: The reality is we will. There's always good news at some point, but the most difficult thing is to try and pick when that is.

JJ: There's a lot of investors that have come into the market that possibly don't necessarily know exactly what they're doing, and they're seeing what they think are bargains that might just go ballistic at some point in time. What is your advice to those people?

RN: I think you've got to do an enormous amount of due diligence and research into those companies, and you've really got to look at what it is that's going to drive their earnings higher over the next few years. If you can't come up with a compelling enough reason that those earnings are going to be able to increase, those stocks have got to be looked at very cautiously. It might be so in the case of the banks. The banks have a lot of provisioning to do, they've been under enormous pressure since the Royal Commission. The focus now has got to be back on the customer, as opposed to the last 20 years, where it's been on the shareholder and shareholder returns. And in some cases with the banks, it's been shareholder returns at any cost. And any exposure to create revenue, even in dealing in areas that perhaps many directors of some of those banks weren't even aware of.

Even airline stocks, for example, we can't just assume that airlines are going to fly and behave in the same way that they did beforehand. People will be a lot more conscious about sitting closely to other people on planes, and the fact that airlines are going to have to spend a lot of money to make sure that that environment is clean and protected, and ensure that people don't get on planes that are sick. So perhaps airlines may be attractive because their share price is cheap, but they may not be the place to invest in, because they're going to have to change their paradigm and perhaps deliver something that's quite different. Even the seating formations might need to change, which would be a big capital cost for companies like Qantas and Boeing, in the US, to change for it to be acceptable.

That's going to play out over the course of the next six to 12 months.

And the other thing that's happened too is people have been forced, in the last couple of months, to embrace the digital age, and technology, which has been available to us. There are so many benefits now to be able to use technology, like Zoom, for example, for meetings, that maybe you don't need to be jumping on an aeroplane and flying to Sydney in the first instance. So I think once people change habits, and behave in a different way, they may not go back to the way they did business before.

We are facing a huge paradigm shift.

In part 2 of our interview with Rod North, we look at further impacts of COVID-19 on the economy and the stocks to watch as we come out of the pandemic.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.