Nick Scali you’ve done it again

Published 10-AUG-2017 13:50 P.M.

|

4 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

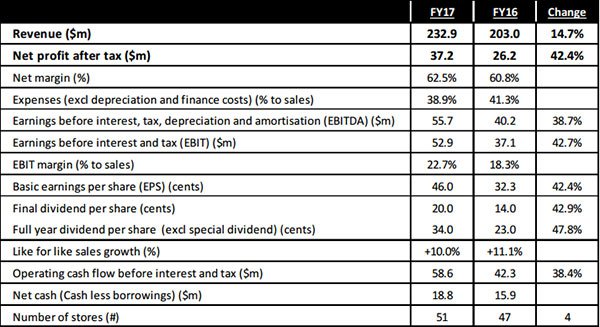

Furniture retailer, Nick Scali (ASX:NCK) delivered an impressive result on Thursday morning which featured 42% net profit growth on the back of a 14.7% increase in revenues. The outperformance of earnings over revenues was reflected in net margins which improved from 60.8% to 62.5%, metrics which most retailers can’t match.

Growth was driven by a mix of increased revenue from new stores (4) and organic growth from its established network. Same-store sales growth of 10% is a healthy sign at a time when there could be a tempering in the rollout of new stores given tentative sentiment towards bricks and mortar retail operations.

Once again, the company demonstrated stringent financial discipline, driving down operating expenses as a percentage of sales from 41.3% in fiscal 2016 to 38.9% in fiscal 2017.

NCK has established a record of being a consistent outperformer and this result should get a tick of approval from analysts as the net profit of $37.2 million was ahead of consensus of $35.4 million.

As a further means of comparison, analysts at Citi were slightly above consensus with their net profit estimates sitting at $36.5 million, but still shy of NCK’s bottom line.

The declaration of a final dividend of 20 cents per share also surprised on the upside (consensus final dividend forecast was 17 cents), bringing the full year dividend to 31 cents.

Key metrics for fiscal 2017 including year-on-year comparatives were as follows.

In commenting on the company’s performance, Managing Director, Anthony Scali said, “Although our overall performance has been underpinned by the current favourable market conditions, I am pleased with the gross margin percentage increase and expense percentage decrease which have both contributed to another record profit result.”

Whether this continues remains to be seen, as such investors should, as always, take a cautious approach to any investment decision made with regard to this stock.

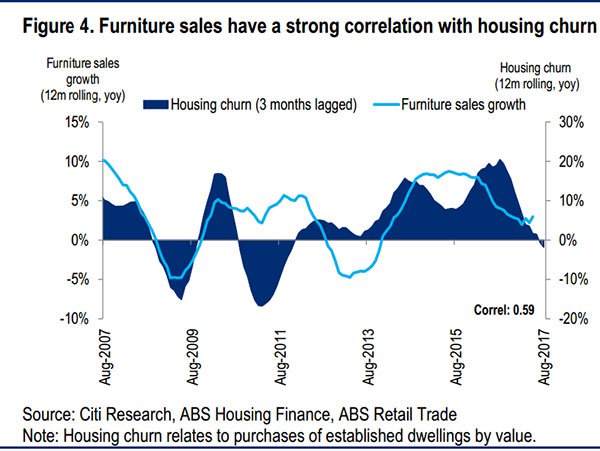

Scali highlighted that the furniture market is directly influenced by consumer confidence, interest rates, unemployment levels and the volume of home renovations and housing sales. Given the slowdown in housing sales expected by some analysts, Scali said same-store sales order growth in fiscal 2018 could be challenging.

These trends are highlighted below.

It is worth remembering though that NCK has negotiated these cycles well in the past as indicated by the consistent strong performance of its share price over the same period reflected above.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Strong balance sheet provides management with plenty of options

Scali reminded investors that the company has a strong balance sheet with a healthy net cash position of $18.8 million, enabling the company to continue its growth strategy and take advantage of any opportunities that may arise.

Some analysts have suggested that the company may put its balance sheet to work by acquiring new brands/stores should negative market conditions result in compelling value propositions.

In the absence of acquisitions, management could employ other capital management initiatives such as the payment of special dividends (as it did in the first half of fiscal 2017) and/or a share buyback program which would have a positive impact on earnings per share.

Based on Wednesday’s closing price of $6.66, the company is trading on a forward PE multiple of 14.7 relative to Citi’s fiscal 2018 forecasts.

Although analysts forecasts are speculative and may not be met.

Given NCK’s growth profile and the strength of its balance sheet this appears to be a conservative multiple. However, taking into account the sense of negativity towards bricks and mortar retailers, the quality of today’s result may not be fully realised.

Having said that, the company is responding well to the emergence of online retailing, coordinating the relationship between the online and off-line customer journey for a seamless brand experience as indicated below.

It is worth noting that even prior to the release of this result, the company was trading at a significant discount to the consensus 12 month price target of $7.81.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.