Investing part 3: Taking advantage of heavily sold off stocks

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

However, as we outlined, these companies have been supported on what investors view as a positive risk/reward basis, and as they progress towards discovering that new oil field or developing that wonder drug they are the same investment proposition today as they were before the advent of the coronavirus.

The five companies we examine today are different in that they all generate revenues and were profitable in the most recent reporting period.

Furthermore, they were forecast to build on those profits throughout the rest of fiscal 2020.

However, with the prospect of supply chain disruptions, business closures and dormant consumer activity most stocks will be affected to some degree.

Key aspects I looked for when choosing the following five stocks were conservative valuations and the capacity to pay dividends.

You will see that most of the companies are trading on PE multiples lower than 10 with a number of them offering yields between 5% and 10%.

Acrow (ASX:ACF)

Acrow Formwork and Construction Services Limited - ACF

Acrow (ASX:ACF) has been active in the Australian construction industry since 1950 and its heritage dates back to 1936 when it first launched in the United Kingdom.

The company generates a significant proportion of its income from the hiring of formwork and scaffolding systems to large construction and civil infrastructure providers across Australia, operating a network of formwork and scaffolding branches in six states and employing approximately 240 people.

The business services a diversified customer base of approximately 1,300 customers, with about 68% of revenues generated by the formwork division and the remainder flowing from scaffolding.

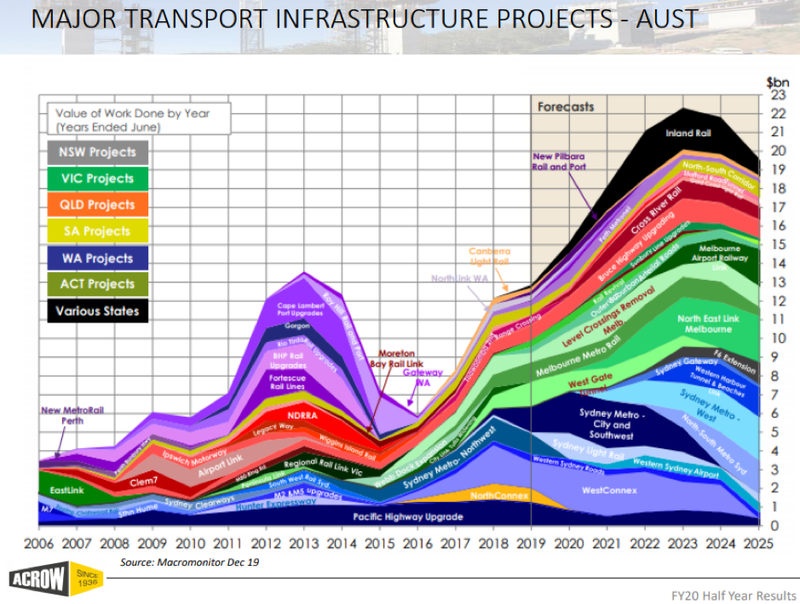

Acrow’s market positioning is important to understand as it generates a substantial amount of income from civil and commercial work, a factor that could stand it in good stead if the government decides to stimulate employment growth by investing in the construction sector, a measure that has been used over decades in responding to economic crises.

Management’s strategy has been to build a business which is diversified nationally, providing defensive qualities, another factor that should work in favour.

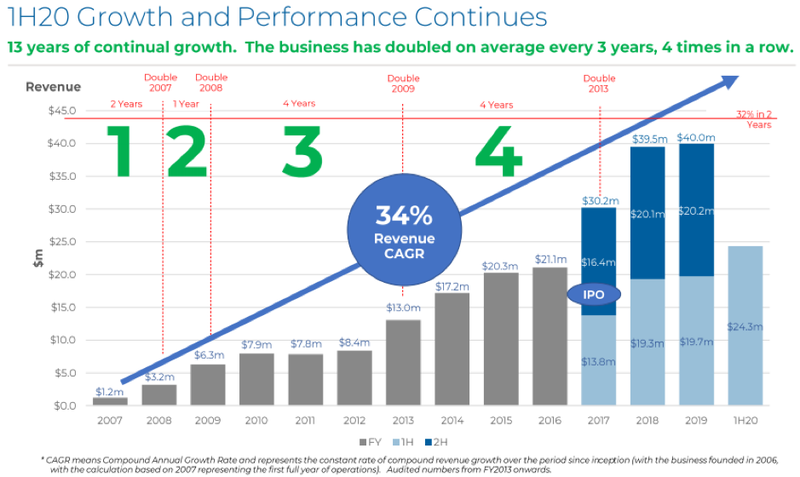

In the second half of 2020 the group will be building on a strong performance for the six months to December 30, 2019.

During this period the group grew underlying earnings by 15% with its operating cash profit up 36% to $4.4 million.

The period also featured the acquisition of Uni-span which is performing in line with expectations as it is positioned to achieve annualised integration savings of up to $2 million in fiscal 2021 while contributing around $5 million to EBITDA.

Uni-span has highly complementary products and services enabling it to provide opportunities across a diversified client base, as well as broad geographic regions and industry segments.

It also brings key relationships in the Australian mining, energy and industrial sectors to greatly complement Acrow’s existing client base.

Acrow experienced strong growth in the six months to June 30, 2018 in terms of total hire revenue and new contracts won, a reliable lead indicator in relation to future revenues.

The following snapshot of the company’s financial metrics demonstrates its resilience despite cyclical industry trends, while also highlighting its robust growth profile.

With significant activity in the civil infrastructure sector planned over the next five years (see below), Acrow should have numerous opportunities to grow its workbook, and this has already been evidenced by the award of substantial infrastructure related contracts in New South Wales and Victoria.

Analysts at Bell Potter liked the look of the group’s first half report, and in early March the broker upgraded its recommendation from hold to buy and increased the 12 month share price target of 32 cents to 34 cents.

After the recent sell-off in the company’s shares this implies upside of 70%.

Based on Bell Potter’s fiscal 2020 earnings projections, the company is trading on a PE multiple of about 4.5, extremely conservative given the broker is forecasting earnings per share growth of 20% in 2021.

Acrow also shapes up as a strong yield play with Bell Potter forecasting a dividend of 1.9 cents in fiscal 2020, increasing to 2.3 cents in fiscal 2021, with the latter implying a yield of more than 10%.

Apiam Animal Health Limited (ASX:AHX)

Apiam Animal Health (ASX:AHX) is a vertically integrated animal health business providing a range of products and services to production and domestic animals.

The company provides veterinary services, ancillary services, genetics, wholesale and retail of related products, together with technical services related to food-chain security.

The farming industry has experienced its challenges due to fires and drought conditions, but management recently highlighted that the group’s robust business model which provides significant diversification has assisted it in responding to industry volatility that can occur in regional and rural operating regions.

In particular, in the first half revenues remained resilient as the company experienced growth from its feedlot, companion animals and acquisitions, effectively offsetting the impact of challenges in the dairy and pig market segments.

While year-on-year revenues and underlying profit were relatively flat, margins increased.

Acquisitions continue to form a core part of Apiam’s growth strategy and in the first half of fiscal 2020 the company completed two significant acquisitions in ACE Laboratory Services and Grampians Animal Health.

The acquisition of ACE Laboratory Services (ACE) was completed in October 2019 with a purchase price of $16 million (inclusive of $3.6 million of deferred earn-out consideration).

ACE is a highly specialised business that offers autogenous vaccines, as well as diagnostic services for large production animal producers.

It is the market leader in both these segments, and it offers Apiam an attractive product and service extension that can then be leveraged across the company’s large production animal footprint.

Apiam also completed the acquisition of Grampians Animal Health in December 2019 for a total consideration of $4.65 million.

This business is located in Hamilton, Victoria, one of Australia’s largest and most productive sheep farming regions.

The business is comprised of two key operating units being a companion and mixed animal vet clinic and a large animal veterinary consulting business with expertise in sheep and beef, as well as providing pasture and grain analysis and parasitology diagnostics.

Underlining the prospect of underlying earnings growth in 2020, Apiam’s managing director, Dr Chris Richards said, “Apiam has delivered another period of resilient revenue and earnings.

‘’Recent rainfall and favourable commodity prices across all segments is positive for the business outlook in the second half of the financial year.

‘’In addition, the global shortage of meat protein is supporting growth in animal numbers.

“Our diversified business model, new complementary revenue streams and focus on cost efficiencies continue to be the key strategic focus for management in order to deliver earnings growth for our shareholders.

‘’Apiam expects to deliver growth in EBIT in H2 FY20 compared to the preceding half, H1 FY20”.

The company’s shares have fallen from 54 cents to 39 cents in the last month, presenting investors with what appears to be a highly beneficial entry point.

Kelly+Partners Group Holdings Ltd (ASX:KPG)

After releasing its results in February for the first half of fiscal 2020, shares in Kelly+Partners Group Holdings Ltd (ASX:KPG) increased from 83 cents to 93 cents, but the coronavirus quickly dispensed with these gains, and the company recently hit a 12 month low of 67.5 cents.

While this seems unjustified given the strong performance, once again it could be a buying opportunity for investors judging the company on its merits which can be clearly seen in its interim result.

Kelly+Partners is a specialist chartered accounting network established in 2006, servicing a broad client base, including private businesses.

It has grown from two Greenfield offices in North Sydney and the Central Coast to 21 operating businesses in Sydney, Melbourne and Hong Kong.

In a model not dissimilar to the medical centre approach whereby multiple complementary businesses such as general practitioners, chemists, physiotherapists and a range of diagnostic services practices share a common location, Kelly+Partners has taken the opportunity to introduce additional services or expand its existing practices at sites where it is already established.

The company listed on the ASX in June 2017, and it has been a successful growth by acquisition story.

The combination of a proven business model and specialist operational expertise has worked in its favour in terms of meeting the needs of individual clients, as well as businesses in the small to medium enterprise market segment.

In the first half of fiscal 2020 the company acquired two accounting businesses located in Melbourne and the Blue Mountains.

The acquired entities have contributed two months revenue of $558,940 and are expected to contribute approximately $3.2 million to nearly $4 million in recurring revenue on a full year basis.

Strategically, the Melbourne acquisition achieves expansion into Victoria by moving into an existing site and taking on the holding costs (lease and fitout) that were being borne by the group.

The Melbourne acquisition is expected to contribute recurring annual revenues in a range between about $2 million and $2.5 million, while generating EBITDA of approximately $500,000.

The Blue Mountains acquisition, together with the group’s offices in Penrith and Bathurst, provide a very significant presence in the outer west of Sydney, one of the regions fastest growing markets.

During the first half, the company benefited from the contribution for the full half year from the four acquisitions made in fiscal 2019, being Inner West, Northern Beaches, North Sydney and Oran Park.

The company’s shares are trading a long way short of the consensus share price target of $1.17 which implies upside of about 70%.

Based on consensus forecasts for fiscal 2020, KPG is trading on an extremely conservative PE multiple of 7.2.

Last year’s dividend of 4.4 cents per share should at least be matched in fiscal 2020, representing a robust yield of about 6.5%.

Near-term share price catalysts include the delivery of the group’s full-year result for fiscal 2020, as well as the strong likelihood of further acquisitions which could be priced even more attractively in the current environment.

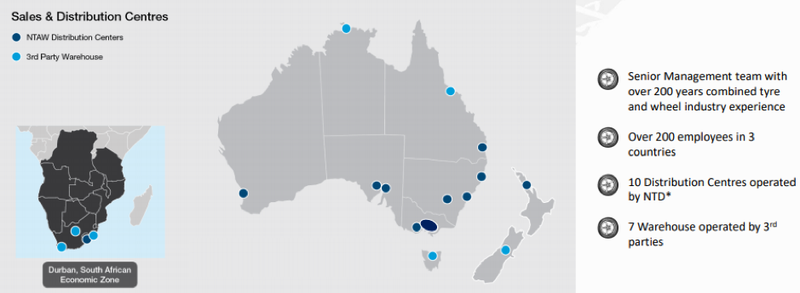

National Tyre and Wheel Limited (ASX:NTD)

National Tyre and Wheel Limited (ASX:NTD) faced some headwinds in the first half of 2020 as the company’s businesses had to contend with competitor discounting.

This resulted in a fall in gross margins, exacerbated by relatively high import prices.

However, the group’s balance sheet remained strong with net cash of $5.3 million, enabling the company to pay an interim dividend of 1.25 cents per share.

Consensus forecasts currently point to a full year dividend of 3 cents per share, but even if the company matches its first half dividend, bringing the full year dividend to 2.5 cents that will represent a particularly strong yield of about 10% based on Thursday’s closing price of 25.5 cents.

The company is still a growth by acquisition story in a market ripe for consolidation.

The other aspect of the business that is worth figuring on the current environment is its resilience in terms of working through a period when consumer spending is likely to be constrained.

Given that the purchase of tyres which normally incorporates tyre-fitting services is a necessity for the motorist, that aspect of NTD’s product offering should hold up reasonably well.

After listing on the ASX in late 2017, the company immediately acquired the assets of Cotton Tyre Service, 50% of TyreLife solutions, a South African importer/wholesaler, 45.6% of the Dynamic Wheel Company that the group did not already own and 50% of MPC Mags & Wheels.

Most recently, the company acquired certain assets from Industrial Tyre Services Pty Ltd (ITS).

These included plant and equipment, intellectual property (including the business name) and some inventory of ITS for the cost or written down value of those assets.

With its head office in Adelaide, Statewide is a leading wholesaler of passenger, van and truck tyres.

Statewide supplies a wide variety of tyres sourced from a large number of suppliers to different customers generally at a lower price point relative to other NTD businesses.

This is significant from a strategic perspective as it should assist NTD in maintaining margins and earnings should ongoing discounting prove to be challenging.

Also, the acquisition of ITS will enable Statewide to establish a branch in Western Australia, which is consistent with NTD’s strategy to diversify its tyre businesses into lower priced segments in new markets.

As the purchase was funded from existing NTD cash reserves, profits won’t be offset by onerous interest payments or earnings per share dilution which would result from equity raisings or share payments to vendors.

Consensus forecasts point to a net profit in the order of $6 million in fiscal 2020, implying earnings per share of 4.2 cents.

Based on these projections the company is trading on a conservative PE multiple of 6, indicating the 40% decline in the group’s share price over the last month is unjustified.

XRF Scientific Limited (ASX:XRF)

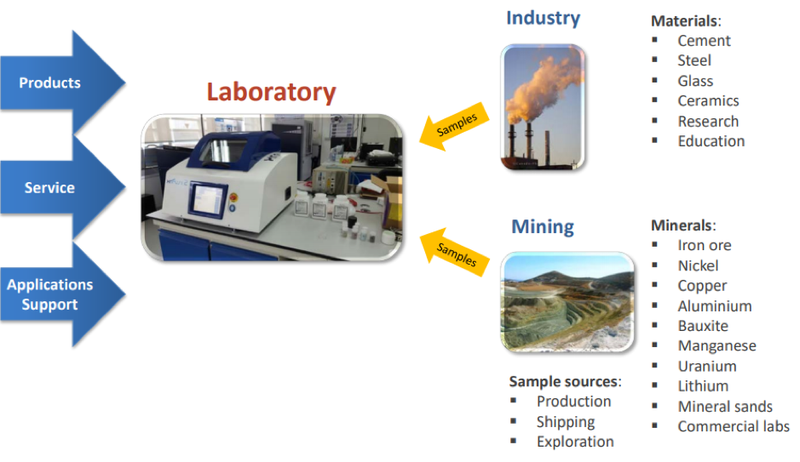

Perth-based XRF Scientific Limited (ASX:XRF) manufactures equipment and chemicals which are distributed to producing mines, construction material groups and commercial analytical laboratories in Australia and overseas.

These are used in the preparation of samples for analysis, an essential tool for mining companies in particular.

XRF has manufacturing, sales and support facilities in Perth, Melbourne, Europe and Canada, but its market reach extends beyond these areas due to its global network of distributors in areas such as the US, South America, Africa and Asia.

The company services most of the large international miners including BHP, Rio Tinto, Vale and Glencore, as well as working in collaboration with other laboratory groups such as the CSIRO and ALS.

The company is often mistaken as one that relies solely on the mining industry, but its technology is used to measure the composition and purity of materials used in construction and the manufacturing of chemical and petrochemical products.

XRF delivered underlying revenue and earnings growth of approximately of 5% and 40% respectively in the first half of fiscal 2020.

Management is forecasting further profit growth for the full year after delivering a net profit of $1.6 million which equates to 1.2 cents per share.

Consensus forecasts currently point to earnings per share of 2 cents in fiscal 2020, increasing 30% to 2.6 cents in fiscal 2021.

XRF has a consistent track record when it comes to paying dividends, and the return of 1 cent per share for the first half represented a good start to the year.

However, management said it would not pay a dividend in the second half, but the first half dividend still represents a robust yield of about 6% based on Thursday’s closing price of 15.5 cents.

Once again, the extent to which XRF has been sold down appears to be unjustified given its strong growth outlook and the implied PE multiple of 7.8.

From an operational perspective, the consumables division had an excellent half, generating $4.8 million in revenue.

In a buoyant gold environment, the precious metals division delivered a strong result with a $1 million increase in revenues and pre-tax profit up by 58% to $710,000.

Management provided an overview of its plans for 2020, particularly underlining its strategies in expanding the precious metals division and continuing its expansion into new geographic regions.

There are also plans to acquire a greater share of the consumables products market segment, and management has flagged its intention is to pursue merger and acquisition opportunities that provide complementary manufacturing benefits in the laboratory supply or precious metals sectors.

XRF should also benefit from its internal product development in 2020 as it releases two new capital equipment products throughout the year.

Interestingly, XRF’s consensus valuation was revised by analysts in the midst of the CVD downturn, and it stands at 33 cents per share, more than double the company’s current share price.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.