PKP: World Famous Rapper/Actor Ice Cube’s Cannabis Brand FryDay signs deal with our microcap Investment PKP - for USA weed drink manufacturing.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 17,710,000 PKP Shares at the time of publishing this article. The Company has been engaged by PKP to share our commentary on the progress of our Investment in PKP over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Know who this guy is?

West coast gangsta rap royalty...

NWA - Straight Outta Compton

12 solo studio albums - many of which arguably defined 90s and 00s music.

Known by hundreds and millions of people around the world.

How about the biopic "Straight Outta Compton”...

Or the 1997 classic horror/adventure film Anaconda?

He has 30M+ followers on instagram.

Okay fine...

It's rapper, turned writer, turned actor and more recently, turned cannabis entrepreneur...

Ice Cube.

Back in 1995 he co-wrote and starred in arguably the most famous "weed movie" ever - Friday.

(remember watching that with your mates in high school, ahem... unsupervised while your parents were out of town? “You got knocked the F out, man!”, “Bye, Felicia”, “I like pigs feeeet”)

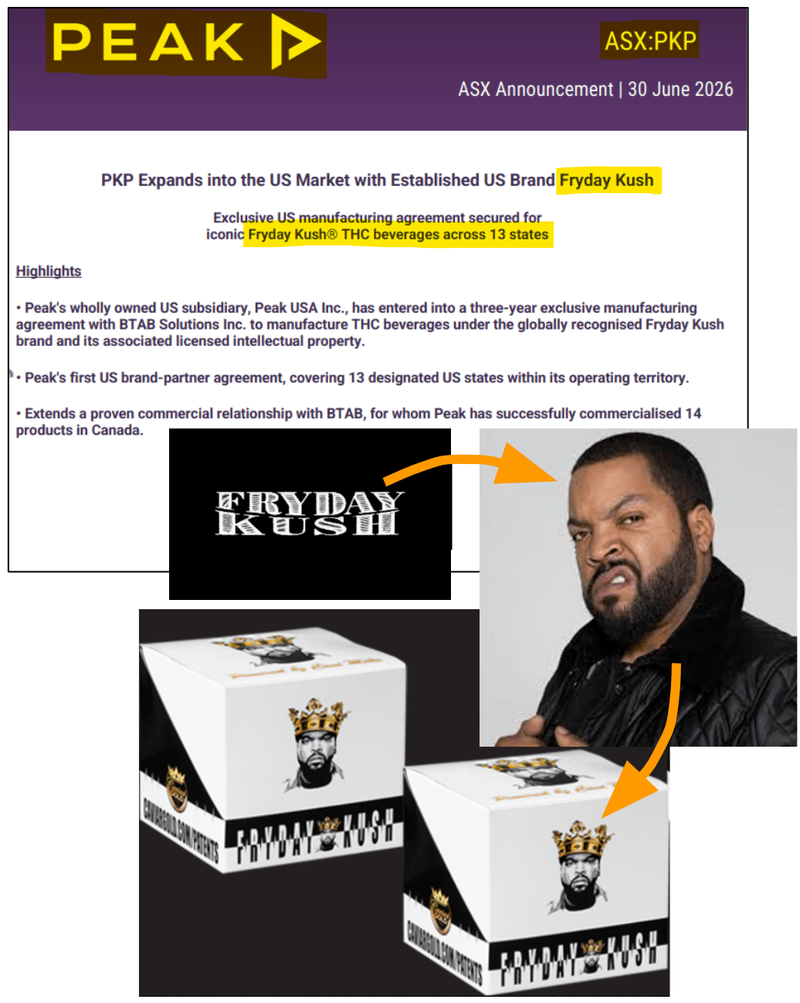

In 2021, Ice Cube turned that Friday movie franchise into his own cannabis brand - Fryday Kush. (source)

(source: just google “who owns Fryday Kush”)

The Fryday Kush brand name is highly recognisable in the cannabis world - it currently operates as an infused flower, moon rock, and vape brand.

In a Forbes interview last year Ice Cube said:

“I used to drink, but once I found good weed, I started pushing the (alcoholic) drinks away. I don’t really like to drink (alcohol) no more.” (source)

And now Ice Cube’s business empire is moving into THC (cannabis) drinks.

In the USA.

But which company is going to manufacture these THC drinks for Ice Cube’s FryDay brand in the USA?

Our microcap Investment Peak Processing (ASX:PKP) is.

PKP owns and sells the technology to "infuse any drink with THC” and then manufacture the drinks at scale.

PKP’s THC-infusion can be applied to ANY drink, so any big alcohol company OR drink maker can use PKP to make a non-alcoholic, THC-infused version of their popular brands.

TODAY: PKP announced that they will be manufacturing Ice Cube's Fryday Kush THC drinks.

In the US, across 13 states.

Pennsylvania, Illinois, Virginia, Ohio, Massachusetts, New Jersey, Nevada, New York, Michigan, Maine, Vermont, Connecticut and Rhode Island.

(This deal is a big validation point of our blue sky thesis with PKP on expansion of its successful Canada operation into the giant USA market)

(source)

PKP is the market leader in Canada manufacturing ~33% of all cans produced for ~70% of the brands in the market.

PKP’s Canadian business is established and profitable.

(more on the Canadian operations in a second)

The “moonshot” for us with PKP has always been replicating its market leading model in Canada into the much bigger US market.

(imagine having 33% market share in a mature US market)

Back in September 2024, PKP opened up a manufacturing facility in Florida. (source)

By August 2025 PKP had its “EnvisionTM Emulsions technology” up and running in Florida, too.

(EnvisionTM is PKP’s tech that makes THC tasteless and mixable - so it can go into any drink)

So PKP entered 2026 fully equipped to showcase its offering to potential US customers.

(and start fulfilling orders)

In H1 FY26, PKP had already sold 680,000+ cans in the US market - including a deal with one of Florida's most established craft brewers (Funky Buddha).

AND after today, that same facility can start manufacturing Ice Cube’s drink too...

A few instagram posts from Ice Cube (where he has 30.1M followers) promoting the drink and who knows how many units get sold...

PKP did ~$3M in cash receipts on 1M units produced last quarter. (source)

So a few million units from Ice Cube’s brand would be material to the company's revenue run rate.

The bigger impact could come from this deal opening the door to other deals...

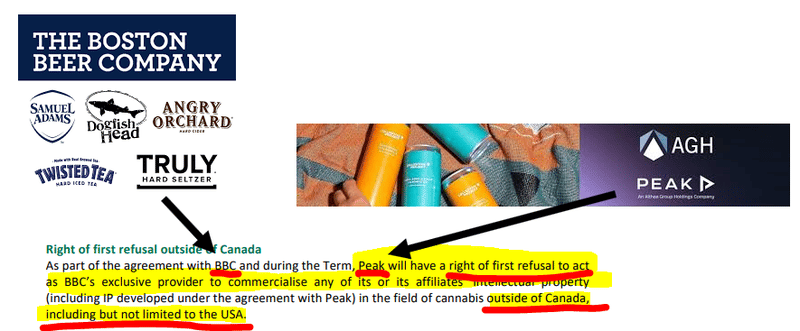

We already know PKP is working with some of the big alcohol companies - like $2.8BN Boston Beer Co.

(currently only in Canada with Boston Beer Co, we are hoping to see them expand to the USA)

Boston Beer Company generated ~US$2BN revenue last year and is best known for: (source)

- Samuel Adams (craft beer)

- Truly Hard Seltzer

- Twisted Tea (alcoholic tea)

- Angry Orchard (hard cider)

- Dogfish Head (craft beer)

- Hard Mountain Dew (in partnership)

The big one for them is “Twisted Tea” which sold 33 million cans in 2024 and is the best selling “hard tea” with more than 80% market share in the USA. (Source)

PKP partners with Boston Beer Co to make a non-alcoholic, THC-infused version of Twisted Tea for sale in Canada (branded as Teapot).

So far, Boston Beer Company hasn't launched a THC drink in the US...

BUT IF Boston Beer Company decided one day that it DID want to launch in the US - PKP’s partnership in Canada gives them a right of first refusal on contract manufacturing for them in the US. (source)

(Source)

So IF Boston Beer Company decides to launch any THC drink into the US... it could be a game changer for PKP.

Of course PKP isn’t limited exclusively to Boston Beer Company either.

PKP also makes drinks for Organigram - the Canadian cannabis producer ~45% owned by ~$200BN British American Tobacco - plus St. Peter's (Cookies, Green Monké) and Electric Brands (Sweet Justice). (source)

(source)

Again, PKP’s THC-infusion can be applied to ANY drink, so any big alcohol company can use PKP to make a non-alcoholic, THC-infused version of any of their popular drink brands.

IF Red Bull wants to make a THC infused version of their drink they can also do a deal with PKP.

If Pepsi wants to launch a THC version of their drink, PKP can make it happen...

(let’s not forget that in 2018 a few almost entered the space... remember Heineken's Hi-Fi Hops and Constellation Brands (the owners of Corona) taking a position in a Cannabis brand).

We think PKP’s market leading position in the highly regulated Canadian market will also make it the ideal trusted partner for these major alcohol companies to work with.

(and today's USA entry of an early moving, relatively known name helps start the derisking process)

They will be looking for someone with real life delivery experience at scale - so being the market leader in one of the most regulated markets in the world (Canada) will matter.

All we need now is for the current “cowboy” USA THC drinks industry regulations to be changed so the bigger boys in the industry feel comfortable doing major product launches...

(we have an update on the regulatory environment in the US later in today’s note)

Overall, our view is that regulation is bullish for a company like PKP.

IF PKP can make it work (and become a market leader) in a highly regulated market like Canada - then when regulation comes into play, all the drink makers will have a company they know can navigate regulation successfully to call (PKP).

PKP’s Canadian operations are EBITDA positive now too

As mentioned earlier, PKP’s Canadian business is the market leading THC drink manufacturer in Canada.

PKP manufactures ~33% of all cans produced in the Canadian THC drinks market for ~70% of all brands sold in country. (source)

Here are some of the big THC drinks brands PKP has as customers:

(source)

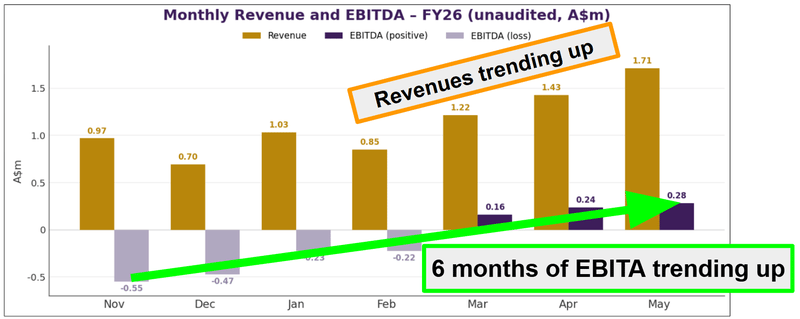

Two weeks ago, PKP reported its third straight month of positive EBITDA in Canada.

(a big turnaround from November last year when the Canadian business was running at ~A$550k negative EBITDA) (source)

Here are PKP’s EBITDA numbers for the past three months:

- March 2026: +A$159k

- April 2026: +A$235k

- May 2026: +A$282k

(source)

PKP’s shown ~A$676k of EBITDA in three months and a trend of that number getting stronger.

May (i.e. last month) was also PKP's biggest revenue month of FY26 at ~A$1.71M. (source)

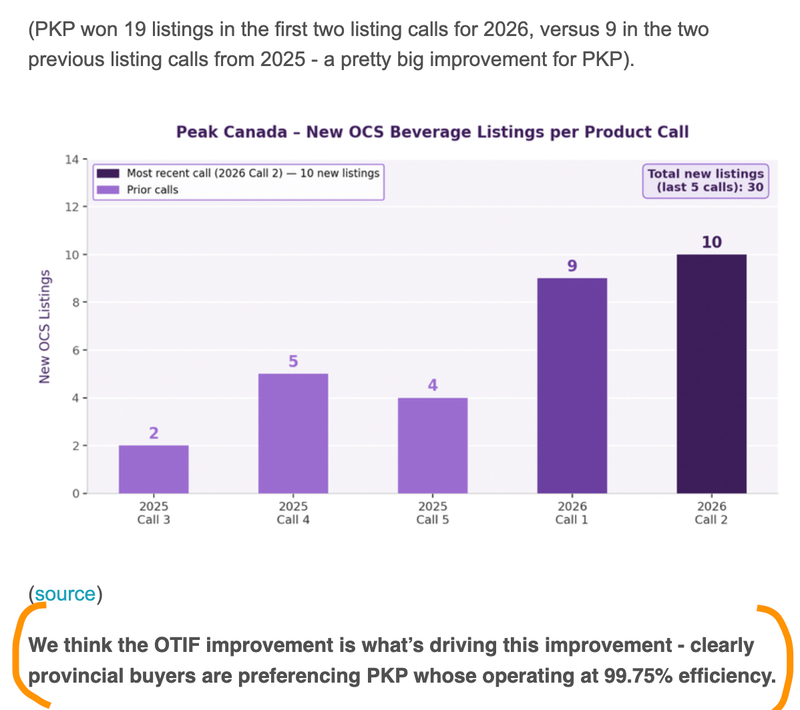

We said in our last note that all the right metrics were improving for PKP to win more and more shelf space in Canada AND that eventually we expected that to flow through to PKP’s bottom line.

It now looks like that is happening.

For context - PKP's "on-time, in-full" delivery score went from 53% (June 2025) to 99.75% (Feb 2026). (source)

(in Canada, THC drinks are bought by centralised provincial distributors - the more reliable you are, the more shelf space you win)

More reliability → more listings → more volume → and finally better financials.

Here is what we said in our last note:

(source)

With 30+ new product listings scheduled to launch between June and September 2026 we are hoping to see the Canadian operations economics get stronger into the end of this year. (source)

(source)

So while we wait for the US moonshot (now helped by early USA market mover Ice Cube) to play out we get full exposure to PKP’s market leading Canadian business.

Ultimately, success in the US will be what leads PKP to delivering our Big Bet for the company which is as follows:

Our PKP Big Bet

“PKP re-rates to a $200M+ market cap on the back of strong THC Beverage sales growth in North America”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including financing risk, regulatory risk, and market adoption risk - just some of which we list in our PKP Investment Memo.

Success will require a significant amount of luck and good management. Past performance is not an indicator of future performance.

What else is happening in the US THC drinks space right now

For the big US moonshot to materialise for PKP there needs to be mainstream adoption of THC drinks.

Right now we are seeing early signs that adoption is coming...

- Target is expanding THC drinks across three more states after a 10 store pilot program in Minnesota (Oct 2025). Now its plan is to roll out THC drinks in 300+ stores in Texas, Florida and Illinois (May 2026). (source)

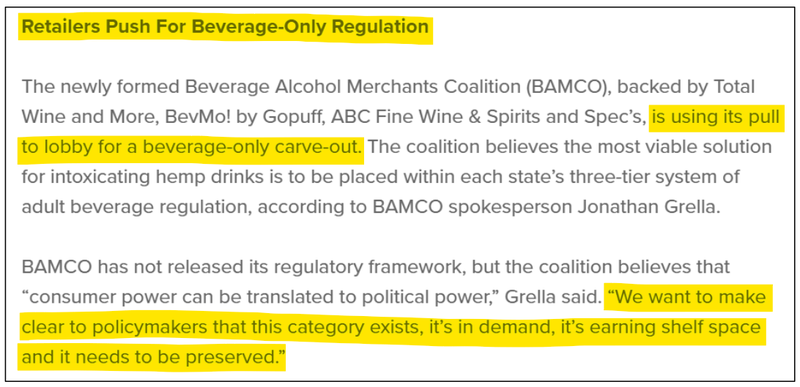

- Total Wine & More is reportedly replacing craft-beer sets with cannabis beverages. (source)

- Circle K plans to sell hemp THC beverages across its US network (where authorised) in 2026. (source)

- Sprouts Farmers Market added THC drinks to ~115 stores across Texas and Florida. (source)

All of that is happening despite a potential US federal ban coming up in November - which to us is a good sign the big guys think regulation will come in before a blanket ban on the sector.

(probably because demand signals are telling them to get into the space)

It’s also nice to see them using their lobbying muscle to try to soften the ban narrative... (more on that in a second)

(source)

US delta-9 THC drink sales were up ~148% year-on-year in the 52 weeks to late February 2026. (source)

Retail sales were about US$250 million, predominantly occurring in liquor (about US$150 million) and convenience (roughly US$56 million) stores.

And US alcohol consumption is sitting near 23-year lows as Gen Z reaches for lower-calorie, no-hangover alternatives.

The big risk (and opportunity) for PKP - and where US regulation is heading

The biggest risk for PKP in the US is regulation.

In November 2025, a new US federal law redefined "hemp" - imposing a hard cap of 0.4mg of total THC per container for finished products. (source)

(Most THC drinks on the US market today contain 2.5–10mg per serving)

So on paper, when enforcement kicks in on 12 November 2026, that law would make the majority of US THC drinks non-compliant.

That's the bear case that we think delays PKP’s expansion into the US.

We are however starting to see a move away from an outright “ban" toward "regulate and delay."

We think regulation is amazing for PKP because it knows exactly how to operate in a highly regulated industry - like Canada where it's a market leader.

So “regulate and delay” could actually be good for PKP.

Here is a quick overview of everything that’s happened which leads us to think the outright ban is becoming less and less likely.

- December 2025 - Trump signed an Executive Order to work with Congress to preserve access to full-spectrum CBD products. (source)

- April 2026 - The federal government rescheduled medical marijuana to Schedule III - the first reclassification off Schedule I in 50+ years. (source)

(This covers medical marijuana, NOT hemp-derived THC drinks directly - for us its a sign the US government is softening its broader “ban” narrative) - April 2026 - US began covering hemp-derived CBD products under Medicare. (source)

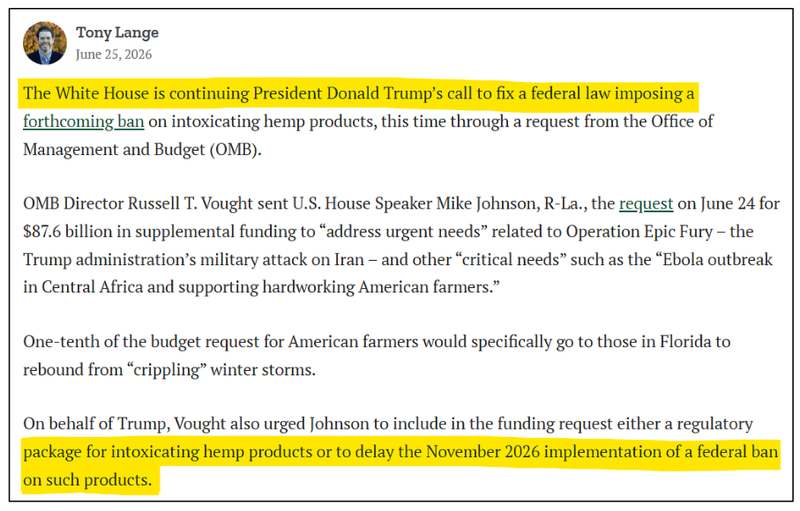

- 24 June 2026 - the White House budget office formally asked Congress to either replace the ban with a regulated framework, or delay it. (source)

That last one happened six days ago...

We think the conversation is moving in the right direction for PKP.

BUT of course there is still a very real risk the ban does go through in November which would materially impact PKP’s US business.

(but it appears Ice Cube and his advisors don’t think so)

So why do we think a regulated US market is actually GOOD for PKP?

PKP already operates in the most tightly regulated THC-drinks market in the world - Canada.

And it’s become the #1 manufacturer in that market (~33% of all cans).

Regulation creates barriers - compliant manufacturing, testing, labelling, licensing all of which is hard to replicate especially in a new sector like THC drinks.

And more importantly, it's even harder to convince a big drink brand to trust you with the launch of their new product, if you haven’t done this at scale before.

We think that if/when the US lands on a regulated framework, the serious brands will need a manufacturing partner they can trust (like PKP).

In business this is called “regulatory capture” - when bigger, compliant incumbent companies welcome (even encourage) regulation because it solidifies their position in the market by making it harder for smaller, non compliant operators)

We think that another positive to come from regulation will be a more certain and predictable environment for the bigger brands to start launching drinks.

The more the industry grows in general the better it will be for PKP...

We could be wrong here - and obviously as shareholders in PKP we are biased.

~Five months to go now until we find out (in November 2026).

Peak Processing

What we want to see next from PKP

There are three things we're watching over the next 6–12 months.

🔄 Operational updates in Canada.

PKP’s Q4 production guidance is now ~1.6M units - we want to see those numbers increase.

- 🔄 Q4 FY26 production: ~1.6M units (confirmed purchase orders in hand)

- 🔲 Improve capacity utilisation.

- 🔲 More new brand partnerships in Canada

🔄 More manufacturing deals signed in the US

Today's Fryday Kush deal is the first US brand-partner contract.

We want to see more of these type deals.

- ✅ Fryday Kush (Ice Cube) - first US brand-partner deal signed

- 🔲 More US manufacturing deals

🔄 US regulatory resolution

And of course the big one - the 12 November 2026 regulatory deadline.

We are hoping to see the US land on a regulated framework (or a delay) rather than a hard ban on the THC drinks industry.

What could go wrong?

The two key risks for PKP right now are regulatory risk and financing risk.

As mentioned multiple times in today’s note the single biggest risk in the medium term is the US federal ban on hemp-derived loopholes that could make most current US THC drinks non-compliant.

IF that ban is put in place then PKP’s US business is effectively halted and we think it could re-rate PKP’s share price lower.

Regulatory Risk

Canada: The THC beverage market is tightly regulated. Any change in Canada’s regulatory environment could disrupt PKP’s ability to produce, sell, or distribute products.

United States: The market operates in a legal grey area under the 2018 Farm Bill, which permits hemp-derived THC (under 0.3% Delta-9 THC). However:

- Several states are cracking down (e.g., Texas is attempting bans).

- Regulatory uncertainty may limit national expansion, with state-by-state laws varying.

- A potential federal reclassification of cannabinoids could change market dynamics overnight.

Source: “What could go wrong” - PKP Investment Memo - 11 July 2025

The second risk is financing risk.

PKP is reporting positive EBITDA months, but there is no guarantees that results in positive cashflows at the corporate level.

PKP also secured a ~A$2.4M loan note in May to fund its Q4 production ramp up. (source)

There is always a chance PKP needs to raise more capital in the future to settle its loan notes OR to fund operations.

Financing Risk

PKP is still in early commercialisation in the US and may need additional capital to expand into new states or marketing spend to build its brands.

In the absence of profitability, PKP may dilute shareholders through capital raises or struggle to fund growth internally.

Source: “What could go wrong” - PKP Investment Memo - 11 July 2025

Other risks

Like any small-cap cannabis technology and manufacturing company, PKP carries significant risk, here we aim to identify a few more risks.

The company's US growth strategy heavily relies on the commercial success of third-party brands like Ice Cube's Fryday Kush. There is always a chance celebrity-backed products fail to gain traction AND major partners like Boston Beer Company choose not to exercise their right of first refusal in the US.

Any unforeseen operational disruptions, equipment failures, or supply chain bottlenecks could impact the company's financial turnaround negatively.

While the US THC beverage sector is currently expanding, it remains a young and highly competitive market segment. There is no guarantee the market grows large enough for PKP to build a viable business in the US..

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our PKP Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

In our PKP Investment Memo, you can find the following:

- What does PKP do?

- The macro theme for PKP

- Our PKP Big Bet

- What we want to see PKP achieve

- Why we are Invested in PKP

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.