GUE: Uranium Enrichment Technology

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,098,352 GUE shares and 500,000 GUE options at the time of publishing this article. The Company has been engaged by GUE to share our commentary on the progress of our Investment in GUE over time. GUE recently changed its stock code from OKR.

Uranium enrichment technology is top secret stuff.

Mined uranium straight out of the ground is one thing...

With a spot price hitting US$100/pound recently, dozens of ASX mining explorers are out there chasing new uranium resources...

ENRICHED uranium is another thing altogether.

This is where it gets really serious.

Enriched uranium is nuclear fuel.

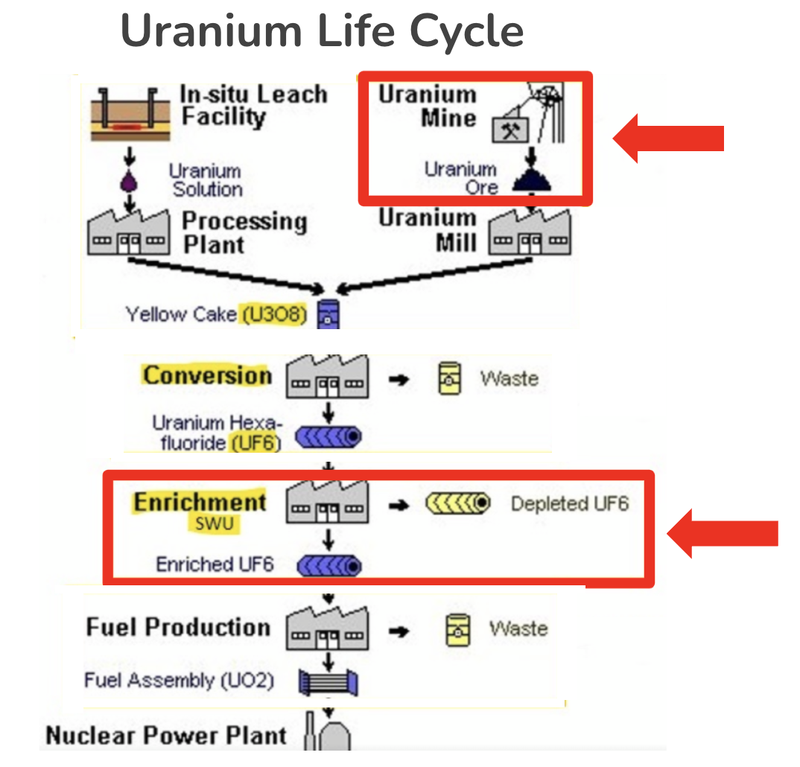

The process of enrichment takes raw uranium mined from the ground (yellow cake) and turns it into nuclear fuel.

Enrichment processes and technologies are closely guarded secrets.

Without enriched uranium, nuclear power plants can't produce electricity.

Russia and China control 63% of the world’s uranium enrichment capacity.

Not ideal in the current geo-political landscape where access to resources and technology are being used to apply pressure.

The US Department of Energy recently made a global call out, via a Request for Proposal, for Enriched Uranium.

Enriched uranium can be used for Small Modular Reactors - an exciting new type of reactor that can be built in a factory and sent anywhere as an emissions free energy source - think mining sites, industrial sites, or small towns.

The US government sees this next generation nuclear power technology as critical, and wants to see a commercial supply chain evolve over time.

Funding of US$700M has been provided under the Inflation Reduction Act (IRA).

There are only two stocks on the ASX that have uranium enrichment technology assets.

One is Silex Systems - which has gone from a 30c share price in 2019 to now $5.12, and a $1.2BN market cap. It owns 51% of its enrichment technology.

The other is another less known, emerging story - Global Uranium and Enrichment (ASX:GUE).

GUE is capped at $25M - a tiny fraction of Silex.

GUE owns a 21.9% stake (and is the largest shareholder) in a private Australian company developing uranium enrichment technology. The private company is called Ubaryon.

We Invested in GUE in February 2023.

(at the time its stock code was OKR, but later changed its code to GUE.)

Today, GUE gave some updates on how its enrichment technology stake is progressing.

In recent months, GUE’s enrichment tech company Ubaryon has:

- Entered an MOU with entX Ltd to evaluate application of Ubaryon’s technology on medical isotopes.

- Developed a novel uranium recovery process which has the potential for significant benefits in environmental waste management, and it looks like it is patentable technology.

- Been investigating numerous funding options, including the recently announced Request for Proposal from the U.S. Department of Energy for Enriched Uranium.

- Applied for Australian Federal government support through an industry growth program.

The most notable updates for us was that Ubaryon was looking into the US$700M available under the IRA’s HALEU program being run by the US Department of Energy and the application for Federal grants here in Australia.

GUE’s cash balance at December 31st was ~$1.1M - which is not enough alone to make any meaningful progress on its assets - so we think that any news on outside funding sources for Ubaryon would be welcomed by the market.

In any event, GUE will need to shore up its balance sheet somehow if it wants to progress its other assets.

For us, any sort of government financing either in Australia or the US would be a strong endorsement of the enrichment tech from AND could put GUE and Ubaryon on the radar of the big enrichment technology players.

That’s where we think the big upside is for GUE - any surprise funding announcement by a government body OR a partnership from a major enrichment company/uranium producer would be completely unexpected by the market.

AND given GUE is the only other enrichment exposure on the ASX behind Silex, any unexpected material news around its enrichment tech could be the big catalyst for GUE’s share price.

So there is plenty to look forward to on the enrichment side of things, but GUE also has exploration/development assets spread across North America...

GUE is also gearing up to drill its US uranium assets

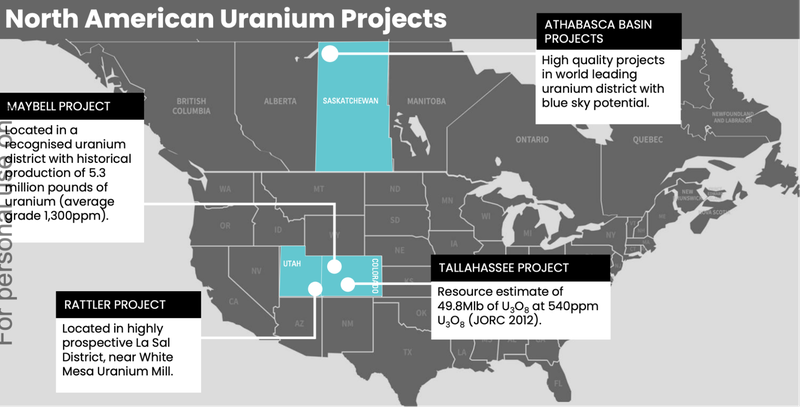

In addition to its stake in uranium enrichment tech, GUE has a portfolio of exploration and development projects spread across North America:

- The Tallahassee project in the US - GUE’s most advanced asset with an existing JORC resource of ~49.8m lb of uranium.

- The Athabasca projects in Canada - Six different exploration assets in the Athabasca basin where some of the world’s highest-grade discoveries have been made/developed.

- The Rattler project in the US - Exploration project in Utah, ~85km away from the only operating conventional uranium processing plant in the USA.

- The Maybell project in the US - a previously operating mine that has produced ~5.3mlbs of uranium in the past. The project has an exploration target of ~4.3 to 13.3m lbs of uranium.

Over the last ~9 months, GUE has been putting all of the permitting together so that it can run drill programs across two of its four projects.

GUE now has permits in place to drill at Tallahassee.

GUE will drill ~20 holes mostly aimed at gathering samples to use for metwork testing that will feed into a scoping study for the project.

Tallahassee is where GUE already has a 50m lb JORC resource, so the focus is less on expanding the size of the JORC resource and more about progressing the project as a potential development asset.

GUE expects drilling at Tallahassee to start in “mid-2024”.

GUE also has permits pending to drill at its Maybell project.

GUE will be looking to drill and convert its exploration target into a maiden JORC resource with 4,600m of drilling over 40 holes.

Drilling is expected in July 2024.

The uranium macro investment thematic is hot - good timing for GUE

The uranium price is still pushing above US$100 per lb - with some of the highest prices it has been since ~2007.

This is primarily driven by a uranium supply crunch.

The biggest uranium producer in North America, Cameco, is planning on ramping up production to meet the supply shortfall, while the world’s biggest producer, Kazapotromon, warned that production growth could be slower than the market is expecting.

Overall, what we are seeing is a modest response to the supply issues across the board at a time when global uranium supply chains are trying to be changed.

Our view is that as long as geopolitical tensions are in play, the supply shortage won't be fixed.

We think that this price action in the uranium market doesn’t consider yet the demand side of the equation, which we think will ramp up over the next decade as countries turn to nuclear energy to meet net zero targets.

With that backdrop, GUE has three major catalysts we think could re-rate its share price higher coming up over the next 6-9 months:

- Drilling and scoping study from its advanced stage Tallahassee uranium project - Here GUE could show the market how close it actually is to getting a project back online - importantly its a project inside the US. The scoping study should also give the market a reasonable idea of the project's economic potential.

- Drilling at its Maybell project in Colorado - here GUE could convert an exploration target into a maiden JORC resource, increasing its US uranium JORC resource base.

- Updates on enrichment technology partner (Ubaryon) - any material news from Ubaryon could surprise the market to the upside.

Progress across the company’s assets and specifically from the enrichment tech partner Ubaryon forms the basis for our GUE Big Bet which is as follows:

Our GUE Big Bet:

“GUE re-rates to a +$250M market cap by achieving a major technological breakthrough with its uranium enrichment technology and/or is acquired at multiples of our Entry Price by a US focussed uranium major looking to gain access to its assets and technology”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our GUE Investment Memo.

Enrichment uranium matters that much more...

The uranium price is now at ~15 year highs and the primary concern in the market is just how fragile uranium supply chains all over the world are.

But a bigger part of the uranium story is how fragile the enriched uranium supply chain is.

First, a quick science lesson, followed by some geopolitics:

Enrichment is a key step that takes raw uranium (yellow cake) and turns it into nuclear fuel.

Uranium found in nature contains only a small percentage (around 0.7%) of the isotope Uranium-235 which can undergo nuclear fission to produce energy.

For uranium to be useful as a fuel in nuclear reactors, it needs to have a higher concentration (3-5%) of the fissile U-235 isotope.

This process of increasing the concentration of U-235 is called uranium enrichment.

Without enrichment, there is no nuclear fuel and nuclear power plants can't produce electricity.

Now, for the geopolitics:

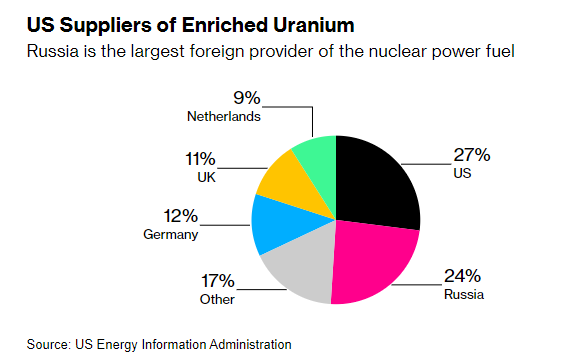

The US has the world’s biggest nuclear reactor fleet (responsible for producing ~20% of US electricity) BUT it produces almost no uranium domestically.

And when it comes to enriched uranium... the US gets ~24% of its supply from Russia.

After the Ukraine/Russia conflict broke out, the US was quick to put sanctions on Russia for things like oil and natural gas, partially, we think, because the US is a net exporter of those products.

For a few months after the war in Ukraine started the US did nothing about the uranium sector...

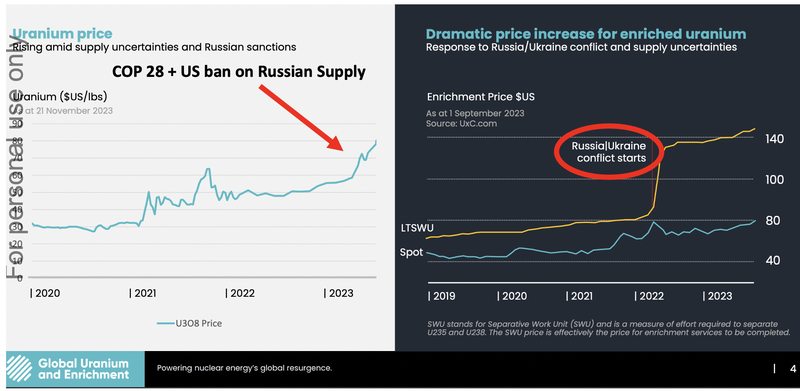

Then late last year, the US government started talking about sanctions on Russian supply.

Almost like clockwork, the uranium price and enriched uranium price started running.

- In late December last year the US House Of Representatives approved a bill that would ban Russian Uranium imports - note the coverage from Bloomberg below mentioned the ban could increase the cost of enriched uranium...

(Source)

- Then at COP28 late last year a pledge was made to triple nuclear energy capacity by 2050.

(Source)

- Coinciding with all of that news, the uranium price really started to run, and enriched uranium prices started to run even harder....

Russia controls almost 50% of the global supply of enriched uranium.

For a long time, the world has been dependent on Russian supply to meet domestic demands.

Western governments are looking to mitigate this supply risk with the US government announcing a US$700M package through the US Department of Energy (DOE) led HALEU program ...

This is a US government attempt to give private enrichment service providers incentives to start building out their own capacity.

Obviously the US government wants the industry to build out capacity, and quickly...

A large part of the reason we are Invested in GUE is because it is one of only two companies developing uranium enrichment technology on the ASX.

The other being $1.2BN capped Silex.

GUE gives us exposure to both uranium exploration and development AND uranium enrichment technology - which we think will be a bigger beneficiary of the macro thematics at play...

Recap - Why we are Invested in GUE

Below are the 8 key reasons why we are Invested in GUE:

1. The US is completely dependent on foreign uranium and uranium enrichment. It’s making domestic uranium assets and enrichment a national priority

GUE has projects across four North American uranium districts, in addition to its 21.9% stake in an enrichment technology company.

We think the combination of technology and assets will make GUE attractive to acquisitive uranium majors and governments as a target of funding.

2. The only other ASX uranium peer with enrichment technology is capped at $1.2BN with 51% ownership of its technology

Silex Systems is GUE’s only “uranium enrichment peer” on the ASX.

Silex has re-rated from a market cap of ~$35M to a ~$1.2BN in the space of two years off the back of US government initiatives, technical advancements and geopolitical factors.

Silex owns a 51% stake in an enrichment technology JV with Canadian uranium major Cameco (who holds the other 49%).

GUE owns 21.9% of its enrichment technology and is currently capped at ~ $25M.

If GUE is able to validate, scale up, and get regulatory approvals for its tech, we think it could follow a similar trajectory to Silex over time as the enrichment technology matures and is proven to work at scale.

3. GUE has an advanced stage 49.8Mlbs uranium JORC resource in the USA

Located in Colorado, USA, GUE’s most advanced US uranium project has a JORC resource of 49.8Mlbs at a grade of 540ppm. Should future drilling be successful here, we think this project could move into a scoping study down the track.

4. Low EV relative to other uranium peers, and none have enrichment exposure

*** GUE has a current market cap of ~$25M and held ~$1.1M in cash at 31 December 2023 giving the company an Enterprise Value (EV) of ~$24M.

GUE currently has a total JORC resource base of 49.8Mlb. On a pure “pounds in the ground”/EV basis, this compares favourably with other ASX uranium peers such as Peninsula Energy (53.6Mlbs, ~$250M EV) and Alligator Energy (53Mlbs, ~$225M EV).

While these two peers are more advanced in developing their assets, GUE is the only one with exposure to uranium enrichment.

5. Highly prospective uranium exploration ground in Canada’s largest uranium producing district

The Athabasca Basin in Canada is home to some of the worlds highest grade uranium projects and produces ~20% of the world’s uranium. We see drilling success in Canada as a significant source of upside if a major discovery is made here.

6. Strong Management and Board, with North America focus

We are impressed with Managing Director Andrew Ferrier’s background in private equity where he was focussed on managing US uranium assets and investments, as well as his degree in chemical engineering.

We think this makes him well suited to understanding the significance of the enrichment technology, and how to get uranium deals done in the US.

We also note the GUE management team’s significant US mining experience and in-country team - this is important for getting projects advanced as quickly as possible.

7. Tight, loyal register

With a relatively low number of shares on Issue, we think the capital structure of GUE is set up well for a re-rate if the company can deliver milestones and/or macro factors bring more market attention to uranium.

8. Advanced stage company

GUE is not just an exploration company - as noted above, it has a JORC stage Uranium project and a major stake in uranium enrichment technology.

This fits with our Investment theme of adding exposure to more later stage companies to our Portfolio, which could begin production sooner in the current commodities supercycle.

What’s Next for GUE

Drilling at Tallahassee project (advanced JORC resource) 🔄

GUE has all of its permits in place to start drilling at its Tallahassee project.

GUE confirmed that drilling here would start around “mid-2024”. We suspect this timing may also be driven by funding position, as we noted above, GUE only had ~$1.1M in cash at Dec 31st.

Drill permits pending for Maybell project:🔄

This week, GUE lodged its drill permits for its Maybell project in Colorado.

This will be the project that gets drilled after the Tallahassee project.

Further updates on uranium enrichment technology (Ubaryon) 🔄

At the fundamental level we want to see Ubaryon de-risk its enrichment technology both operationally and from a regulatory perspective :

- 🔲 Further validation and extend the enrichment performance (show how well it works)

- 🔲 Achieve continuous operation at bench scale (scale up process)

- 🔲 Regulatory approvals

At the same time we are hoping Ubaryon is successful in getting funding either from the Australian Federal government grant or through the US$700M program made available by the US Department Of Energy (DOE) .

What are the risks?

GUE held $1.1M at December 31st 2023, and will require additional funds to progress its projects.

In relation to investors, the biggest risk for GUE right now is ‘dilution risk’ that comes with the company issuing new shares in exchange for funding and a balance sheet that limits the work the company can do.

We suspect the potential for a near term capital raise may be keeping bigger sophisticated investors from buying GUE shares on market because they perceive that they may be able to enter off market via a capital raise.

If GUE wants to move faster, it will need more money. But at the same time, it will likely be hesitant to dilute existing shareholders via the issue of new shares at too low a price.

The way for a share price to move up is by delivering share price catalysts - which typically requires money to do things - so it’s a fine line that all company directors tread when running ASX listed companies.

GUE is planning two drill programs across two different projects in the US and will need a stronger balance sheet to fund both those programs.

Outside of the drill programs GUE also wants to kick off a scoping study on one of those projects meaning there will be costs even after the drilling is completed.

At the moment GUE doesn't have the balance sheet capacity to do all of this work.

GUE will likely need to top up its cash balance either before the first drill program starts OR right after the program gets going.

Our GUE Investment Memo:

Click this link to see our GUE Investment Memo where you can find a short, high level summary of our reasons for Investing.

In our GUE Investment Memo you’ll find:

- Key objectives for GUE

- Why we Invested in GUE

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.